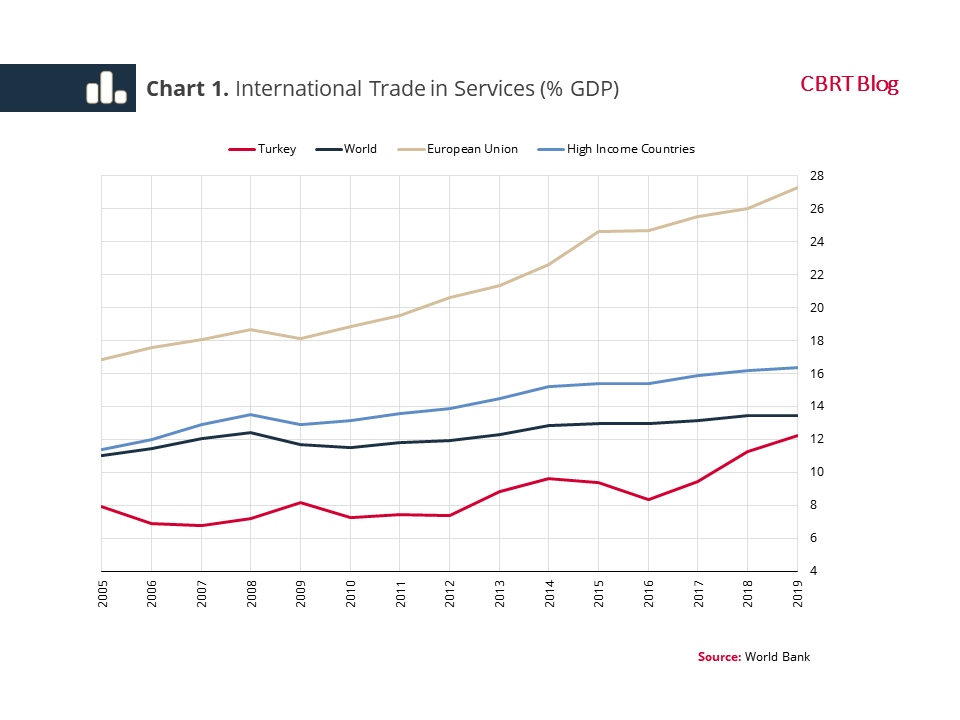

With globalization and digitalization, the share of international trade in services (ITS) in gross domestic product (GDP) has been increasing worldwide (Chart 1). This ratio increased to 13.5% in 2019 from 11% in 2005. In the same period, the growth rate of trade in services in Turkey was above the world average. Turkish ITS, which constituted approximately 8% of GDP in 2005, increased to 12.2% in 2019. This blog post analyzes the structure of Turkey’s exports of services structure based on sectors, relative competition areas and trading markets.

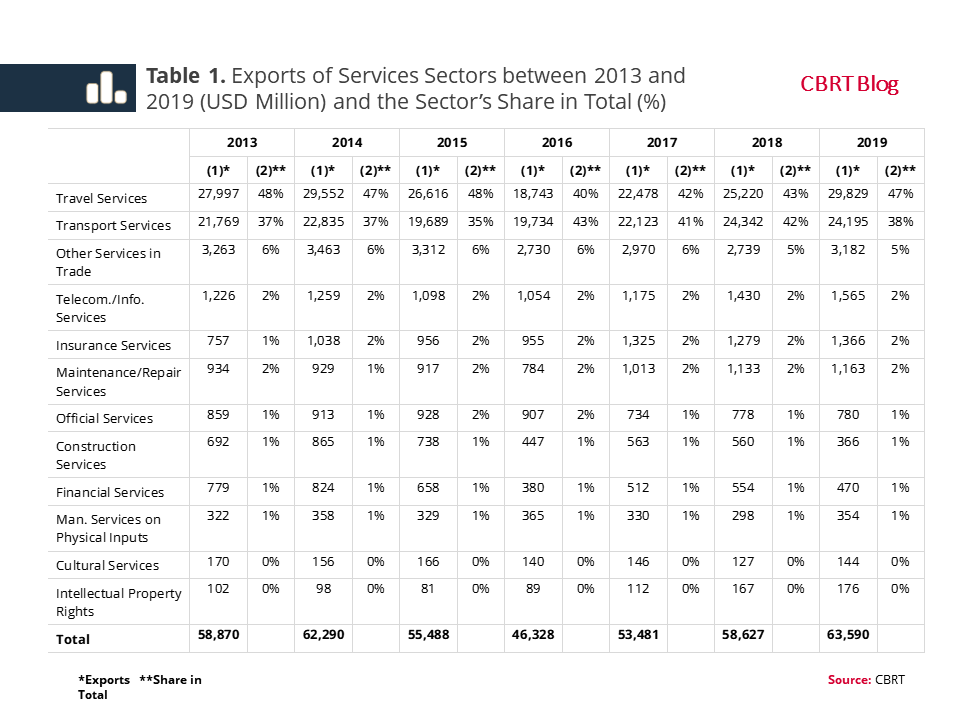

Table 1 shows the development of Turkey’s services exports over the years and the share of sectors in total services exports1. The table shows that Turkey’s exports of services are mostly concentrated in Travel and Transport Services. In the period reviewed, the share of these two sectors in total exports of services was approximately 84%.

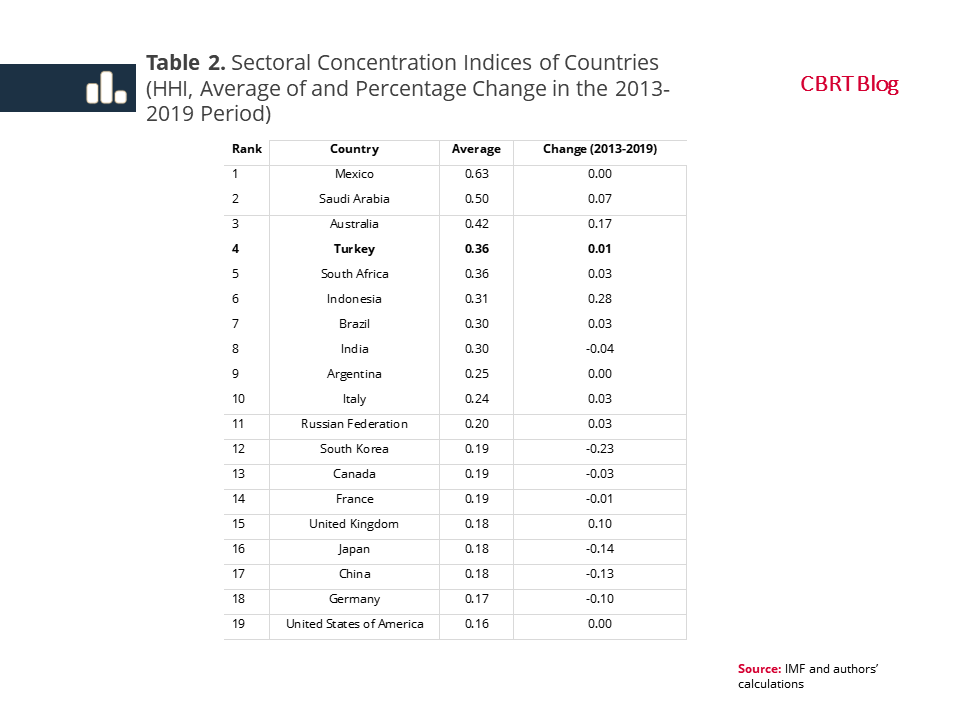

How does a comparison between Turkey and other countries look with respect to sectoral concentration of exports? We can see this by calculating the Herfindahl-Hirschman Index (HHI). The HHI is calculated by taking the square of each sector’s share in total exports of services. A HHI value close to 1 indicates sectoral concentration, and values close to 0.08 indicate a balanced structure2. Table 2 shows HHIs calculated for Turkey and G20 countries3. Turkey, which has an index value of 0.36 in terms of sectoral concentration, ranks 4th among G20 countries. An analysis of the change of sectoral concentration over time suggests that the HHI has decreased in seven G20 countries, and remained unchanged or increased in others. In this period, Turkey’s HHI increased by 1%.

In addition to sectoral concentration, country concentration of exports is also an important structural indicator. Exports of services concentrating on a small number of countries becomes sensitive to geopolitical risks. Country concentration of Turkey’s service exports was measured using HHI for years between 2016 and 20194. Accordingly, Turkey’s average HHI value for 2016-2019 is 0.0377, and it is observed that Turkey’s service exports are evenly distributed among countries.

Sectors that Turkey has Relative Advantage

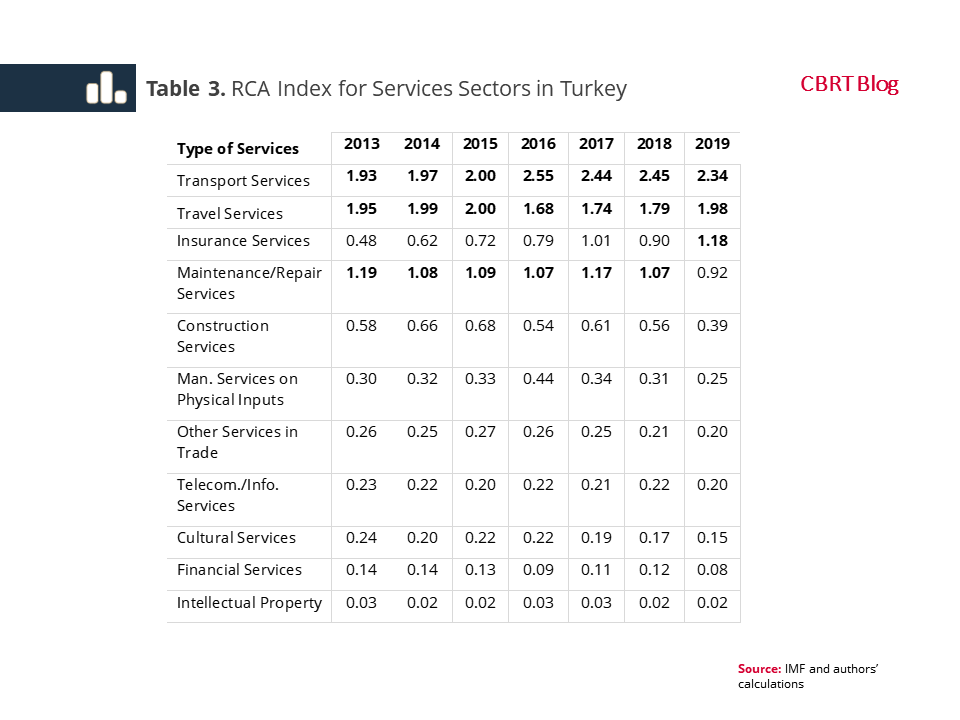

One way to increase our service exports is by focusing on sectors where Turkey has relative advantage and are open to improvement. The Revealed Comparative Advantage (RCA) index provides us with statistical clues with respect to sectors a country is competitive in. The RCA is an index method proposed by Balassa (1965) and is widely used in foreign trade literature5. An RCA index greater than 1 indicates that the country has a relative advantage in a specific sector, while values lower than 1 indicate that the country is not competitive in that specific sector. Table 3 shows Turkey’s RCA index values for 12 sectors for the 2013-2019 period. Accordingly, our country has a high relative advantage in the Travel and Transport sectors. We can conclude that Insurance and Maintenance/ Repair services have moderate relative advantage.

Country Alignment of the Structure of Services Exports

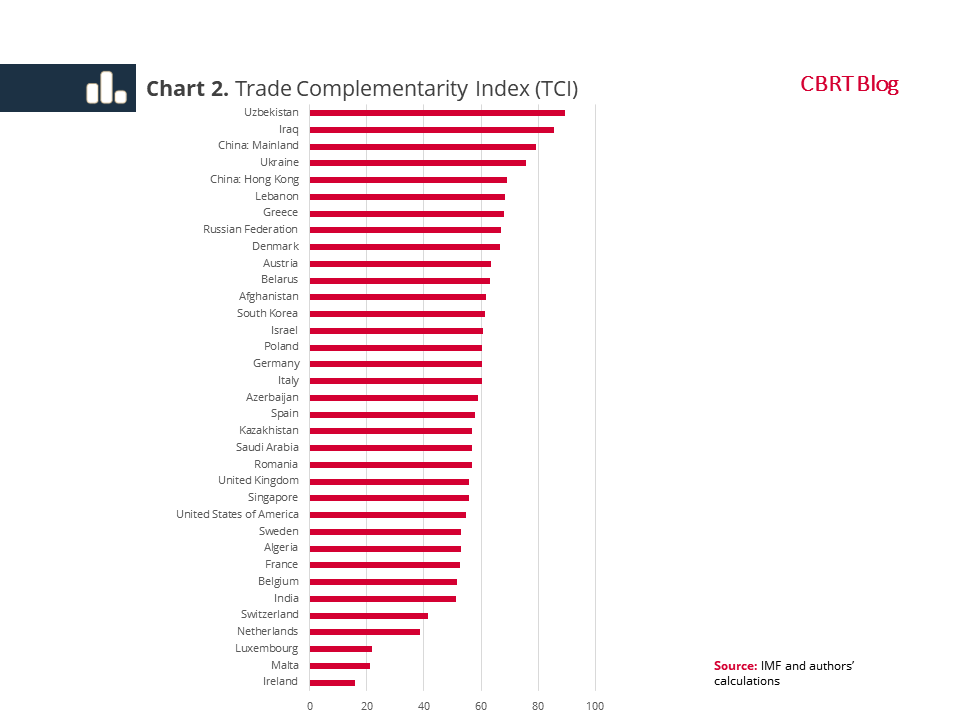

One of the criterion taken into account while choosing a target country to develop exports is to evaluate the similarity between the import structure of the target country and the export structure of the host country. The Trade Complementarity Index (TCI) measures this statistically6. The TTI can take values from 0 to 100. An index value of 100 indicates an exact overlap between Turkey’s export structure with the import structure of the receiving country. Therefore, countries with a high TTI value can be considered as countries with a high services export potential for our country. Chart 2 shows the index values calculated for countries to which we export services. Based on this indicator, Uzbekistan, Iraq, China and Ukraine stand out as countries with high TTI values.

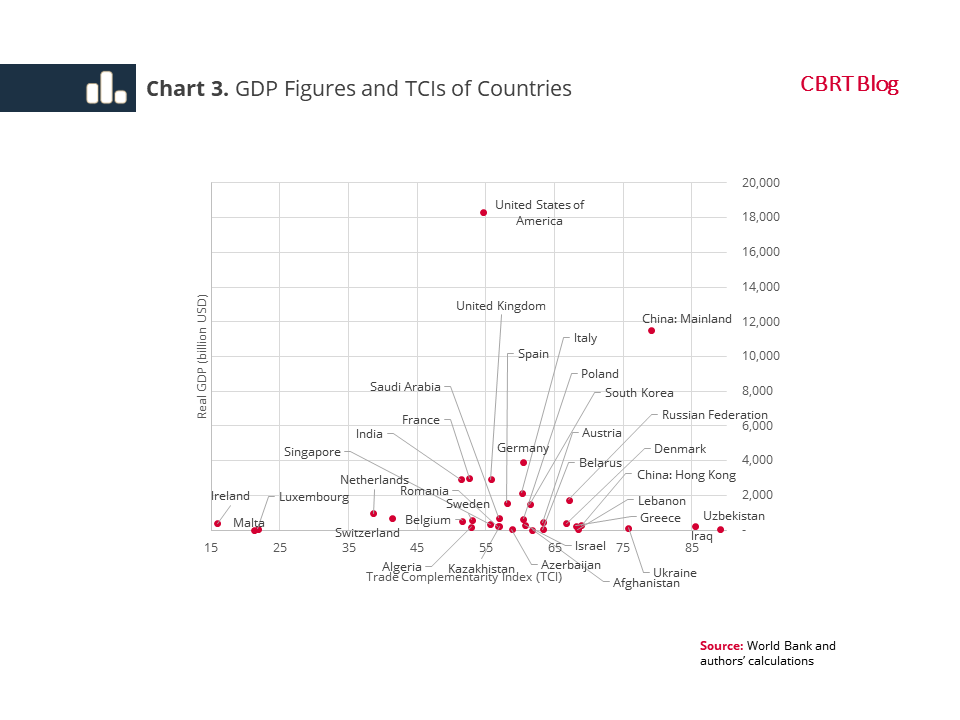

Chart 3 shows the TTI values and GDP of countries. Countries with high TTI value and high GDP will also have high potential or developing trade of services. China, Russia, South Korea, Germany and Italy have high potential with respect to this evaluation.

Conclusion

This blog post evaluated the structure of Turkey’s services exports by using various indicators with a comparative analysis.

An analysis based on sectors reveals that the structure of Turkey’s services exports is dominated by Travel and Transport services. This phenomenon, which is also supported by HHI, creates vulnerability in services exports. As we have observed in the recent pandemic, the balance of services trade can rapidly deteriorate when exports of Travel and Transport services are interrupted.

Although the sectoral intensity is high, services exports show a balanced distribution among countries. This reduces the negative impact of geopolitical developments on services exports.

When the RCA index is taken as an indicator, it is observed that Travel and Transport services have high relative advantage, while Insurance and Maintenance/ Repair services have moderate relative advantage among Turkey’s services exports sectors. While drawing up an exports strategy, it would serve Turkey’s best interests if we focus our export potential on sector with higher relative advantage and design policies to enhance competition in other services sectors.

China, Russia, South Korea, Germany and Italy stand out as countries with high services exports potential for our country, both in terms of size and structure.

1 According to the Handbook of International Trade in Services, trade of services is composed of 12 sectors. ITS categories are as follows: 1. Manufacturing services on physical inputs owned by others, 2. Maintenance/Repair Services, 3. Transport Services, 4. Travel Services, 5. Construction Services, 6. Insurance Services, 7. Financial Services, 8. Intellectual Property Rights, 9. Telecommunication, Information Services, 10. Cultural Services, 11. Other Trade Services, 12. Official Services. The Official Services item whichtbasically covers diplomatic services such as visa services are not considered as a commerical service. Therefore, even if data for these services are included in the study, they will not be included in the analysis.

2 As sectoral concentration is calculated for 12 sectors, the minimum value that the HHI can take is 0.083 when all 12 sectors have equal shares in the total value.

3 HHI values calculated for 125 countries which has data in the IMF database can be accessed here.

4 Due to unavailability of data, the HHI index for 2016-2019 has been calculated excluding Travel Services.

5 The formula defines the share of sector k in exports of services of a country in to the share of sector k in global services trade:

![]()

6 The formula of this idex, which was proposed by Drysdale (1969), is:

![]()

In the formula, i rdenotes exporting country, j denotes importing country and k denotes the sector.

References

Balassa, B. (1965). Trade Liberalisation and Revealed Comparative Advantage. The Manchester School of Economic and Social Studies, Vol. 33, 99-123.

Drysdale P. (1969). Japan, Australia, New Zealand: The Prospect for Western Pacific Economic Integration. Economic Record, 45: 321–342.