The Central Bank of the Republic of Türkiye (CBRT) started to publish the statistics on participation banks’ profit rates for participation accounts and financing (loans) [1] on April 17, 2025 under the heading of “Interest Rate and Profit Rate Statistics”. Profit rate statistics are composed of three different datasets: weekly flow profit rates for participation accounts, weekly flow profit rates for loans, and monthly stock profit rates for loans. This blog post explores the new series, and offers a comparative analysis for the banking sector [2] with the related statistics.

Participation Accounts

Participation accounts are types of accounts in which the funds deposited into participation banks are used by these institutions, and the resulting profit or loss is shared with the account holders.[3] Due to profit and loss sharing, in these accounts, the account holder is not promised a pre-determined return, and the principal sum is not guaranteed to be repaid in full. In this respect, participation accounts differ from conventional deposit accounts. Accordingly, while deposit interest rate statistics show the interest rates applied to newly opened deposit accounts in the relevant week, the weekly flow profit rate statistics display the profit rates realized in accounts closed within the same week.

Chart 1 demonstrates the weekly flow profit rates on Turkish lira (TRY) participation accounts and the weekly flow interest rates on TRY time deposits. It reveals that the two datasets are mostly parallel but profit rates lag behind interest rates during periods when interest rates are elevated. This results from the divergence between the returns on newly opened accounts in the relevant week and those on previously opened accounts that were closed in that week, due to changes in market conditions.

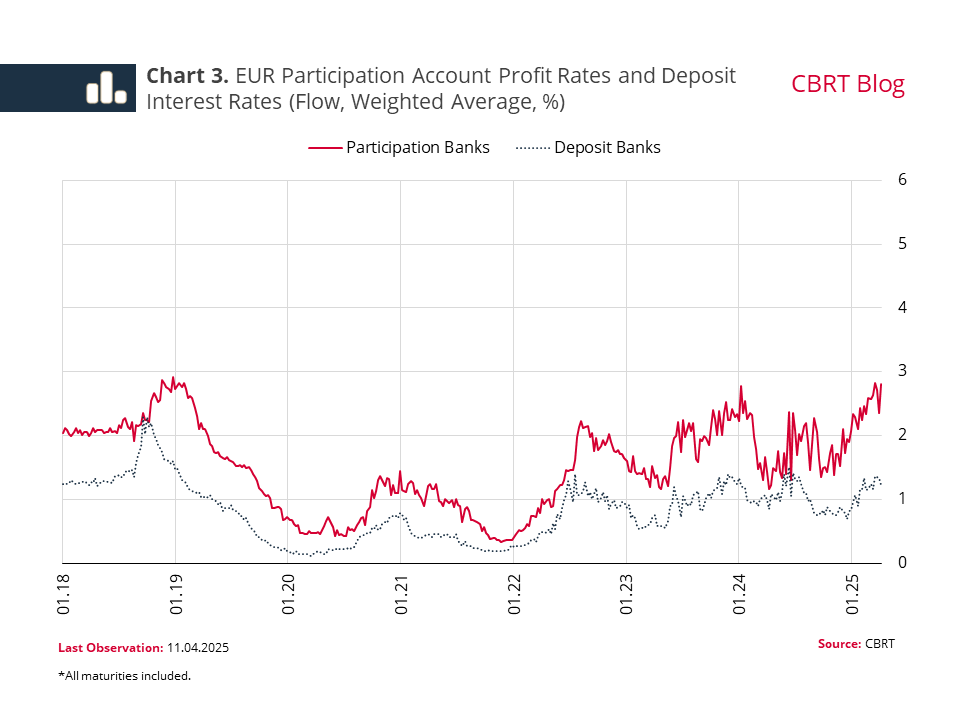

When the same comparison is made for US dollar and euro accounts, it is seen that the rates of return are close in USD deposit and participation accounts, whereas the profit rates are higher than interest rates in euro accounts (Charts 2 and 3).

Loans

Loan profit rate statistics are released in two separate datasets as flow and stock data. Flow profit rates show the rates on new loans extended in the relevant week, and stock profit rates show the rates on all active loans on the relevant date. Unlike profit rates on participation accounts, loan profit rates are determined at the opening of the loans, and therefore, there is no term mismatch when compared with loan interest rates.

A comparison of TRY loan profit rates of participation banks and TRY loan interest rates of the banking sector reveals that both bank groups apply similar rates on commercial loans (Chart 4). However, in the case of consumer loans, the profit rates applied by participation banks are lower, and this gap has significantly widened since August 2023 (Chart 5).

A similar case holds for stock loan profit rates and stock loan interest rates. Stock data covering all outstanding loans reveal that while the rates applied by the two banking groups have remained relatively close in commercial loans, interest rates in consumer loans have historically been higher than profit rates, and this gap has widened since mid-2023 (Charts 6 and 7).

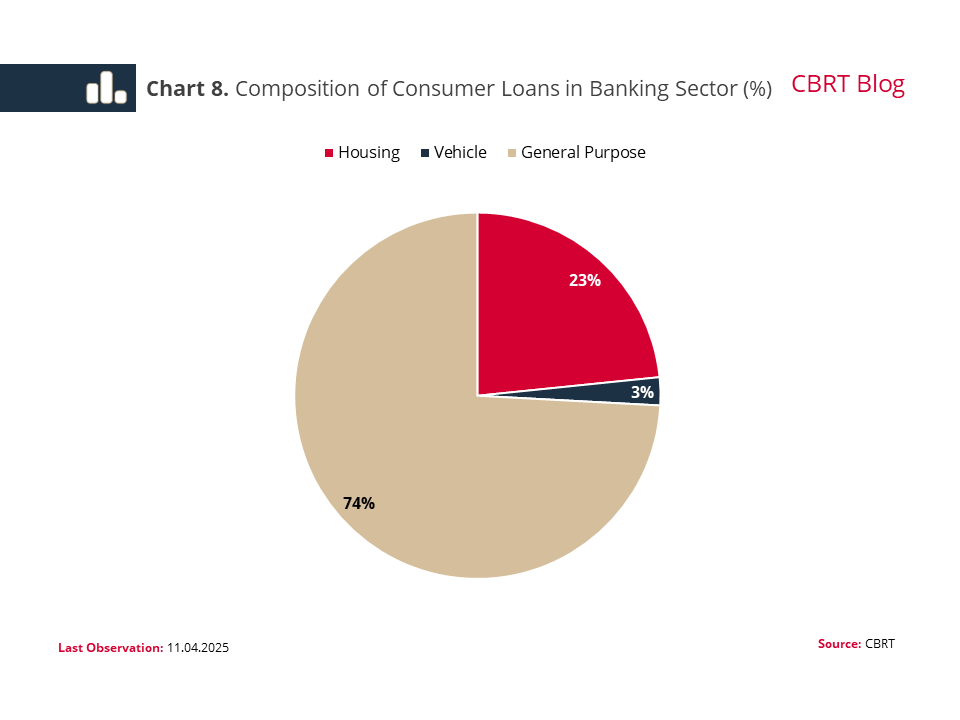

This difference in the rates on consumer loans, which are composed of housing, vehicle and general-purpose loans, is attributed to the differences in the operational nature of participation banking compared to traditional banking. According to the legislation[4], participation banks cannot provide direct cash financing if it is not in exchange for the purchase of a good or service. So, within the scope of general-purpose loans, they offer financing models limited to certain areas such as the Hajj/Umrah pilgrimage, education payments and durable consumer goods, and on the condition that payments are made directly to the seller. Therefore, the share of general-purpose loans in consumer loans is lower at participation banks compared to other banks (Charts 8 and 9). While the share of general-purpose loans in consumer loans is 74% in the banking sector, it is only 17% at participation banks. Additionally, as this financing is made available only against the purchase of goods or services at participation banks, and due to the agreements these banks make with sellers, the profit rates of general-purpose loans remain below the interest rates of general-purpose loans at conventional banks.

In sum, structural differences between participation banks and traditional banks result in a divergence in the returns on funds provided to customers and the cost of loans between the two types of banks. In particular, the differences in the timing of the determination of returns provided to customers in deposit and participation accounts make a direct comparison difficult. This becomes more discernible during periods of significant changes in the degree of monetary tightness. Loan interest rates and profit rates, on the other hand, present a more aligned trend in commercial loans, while they diverge in consumer loans due to the differences in general-purpose lending between the two banking groups.

[1] For ease of comparison with bank loans, hereafter the term “loan” will be used instead of “financing”.

[2] In this blog page, banking sector refers to deposit, development and investment banks and excludes participation banks.

[3] Banking Law No. 5411. (in Turkish)

[4] Regulation on Credit Transactions of Banks. (in Turkish)