To better understand the structure of the domestic debt stock, we need to know which debt instruments are preferred by different types of investors. This information is crucial to identify the risks undertaken by different investors and to understand the impact of possible shocks on the demand for debt instruments. In this blog post, we aim to examine the domestic debt instrument preferences of investors in Turkey and compare them with some selected countries.

Examples from Selected Countries

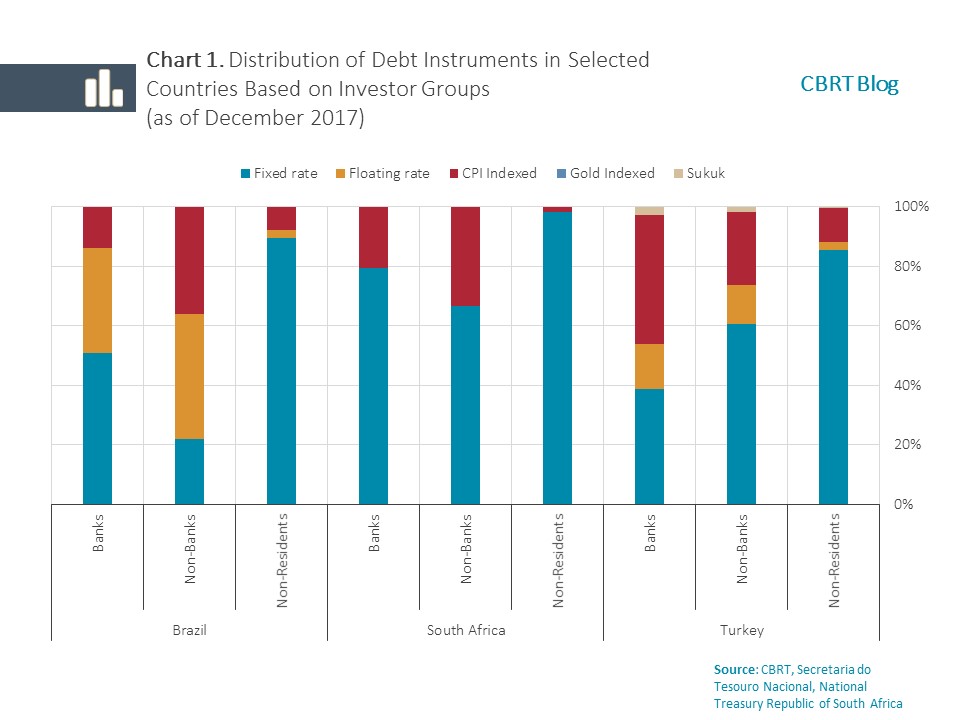

In their debt management reports, countries such as Brazil and South Africa report on the instruments held by domestic debt stock investors. Although these data are less comprehensive[1] than Turkey’s, narrowing the possibility of cross-country comparison, nevertheless examining the distribution of investors’ debt instrument preferences, an important demand side factor for the debt stock, enables a limited comparison[2].

In all three countries, foreign investors predominantly opt for fixed-rate debt instruments (Chart 1). Turkey diverges from the other two countries in that the share of non-resident investors in instruments other than fixed-rate ones is also relatively high. While the debt instrument preferences of the banking sectors in Brazil and Turkey suggest a more balanced distribution compared to South Africa, the weights of floating-rate and CPI-indexed debt instruments vary between the two countries. Non-bank investors are found to opt for fixed-rate instruments in Turkey, similar to the case in South Africa[3].

In sum, foreign investors in Brazil, South Africa and Turkey prefer fixed-rate instruments while instrument preferences of other investor groups vary across countries.

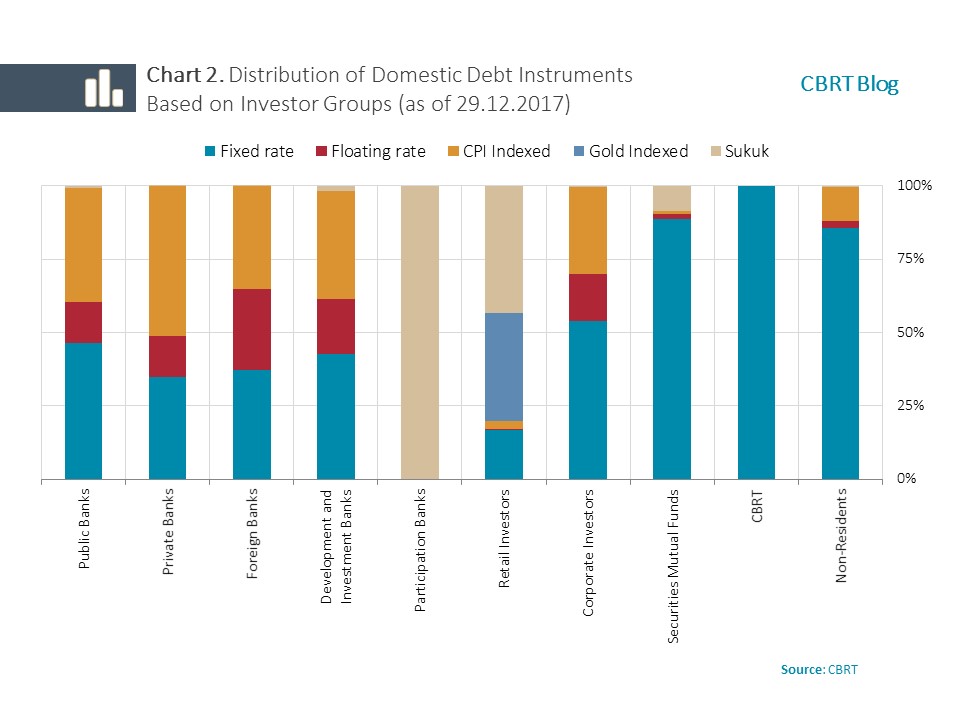

A detailed analysis of the breakdown of domestic debt instruments by investor groups in Turkey reveals that as of end-2017, there were differences between debt instrument preferences of investors that constitute the demand side of the domestic debt stock (Chart 2).

The diversity of instruments preferred by the banking sector is notable. Particularly, a large portion of CPI-indexed and floating-rate instruments are held by banks, possibly to compensate for the maturity mismatch between domestic borrowing and deposits. Meanwhile, participation banks solely invest in sukuk bonds, an instrument in which they also happen to be the major investor. The debt stock of non-bank investors is mostly composed of fixed-rate government bonds.

Measure of Resilience against Shocks

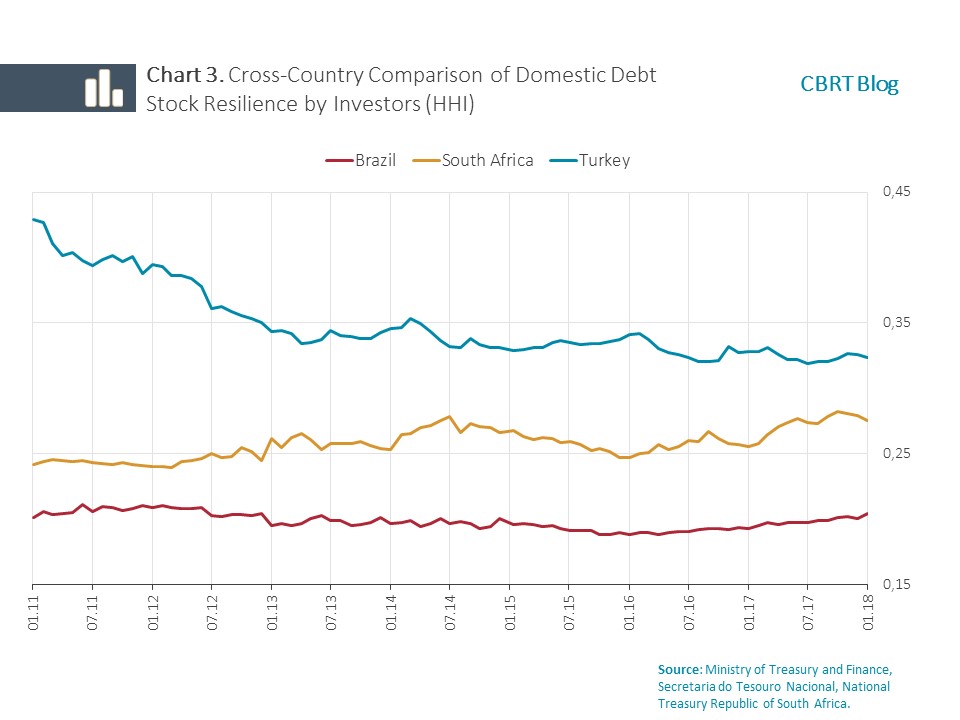

Diversification of the investor base is considered to be a warranty for sustaining a robust demand for government domestic debt securities. Debt instruments data based on investors is important in terms of measuring the resilience of the domestic debt stock against any sensitivity to be posed by changes in instrument preferences of investors. This analysis employs the Herfindahl-Hirschman Index (HHI), a commonly accepted metric for competition among firms and market concentration, as a resilience measure of domestic debt stock[4]. Low concentration ratios in terms of investors or instruments, or in other words, diversification of domestic debt stock across a wider range of investors and instruments, enable the containment of both the investor-specific and the instrument-specific risks.

An HHI value close to zero indicates a variety of investors or instruments in the market, which suggests a balanced distribution. If the index takes values around 1, this implies a monopolistic market structure, which therefore signals high concentration and fragility.

As data sets in selected countries are not compatible with the data set in Turkey, the cross-country analysis of the resilience against shocks is based on the total domestic debt stock concentration in these countries by investors[5]. This concentration is obtained by adding the squares of the shares of each debt stock holder, thereby formulating an HHI for the total domestic debt stock (Chart 3).

At the onset of the analysis period, the concentration in Turkey is higher compared to the other two countries since its banking sector is mainly a domestic debt stock holder. However, over time, this concentration decreases in degree and significantly improves[6]. The lower concentration in Brazil and South Africa is attributed to strong private pension systems (PPS) and lower dependence of these countries’ domestic debt stock on the banking system. In this respect, sustaining the efforts towards enhancing the PPS is crucial to prop up the improvement in the domestic debt stock concentration in Turkey.

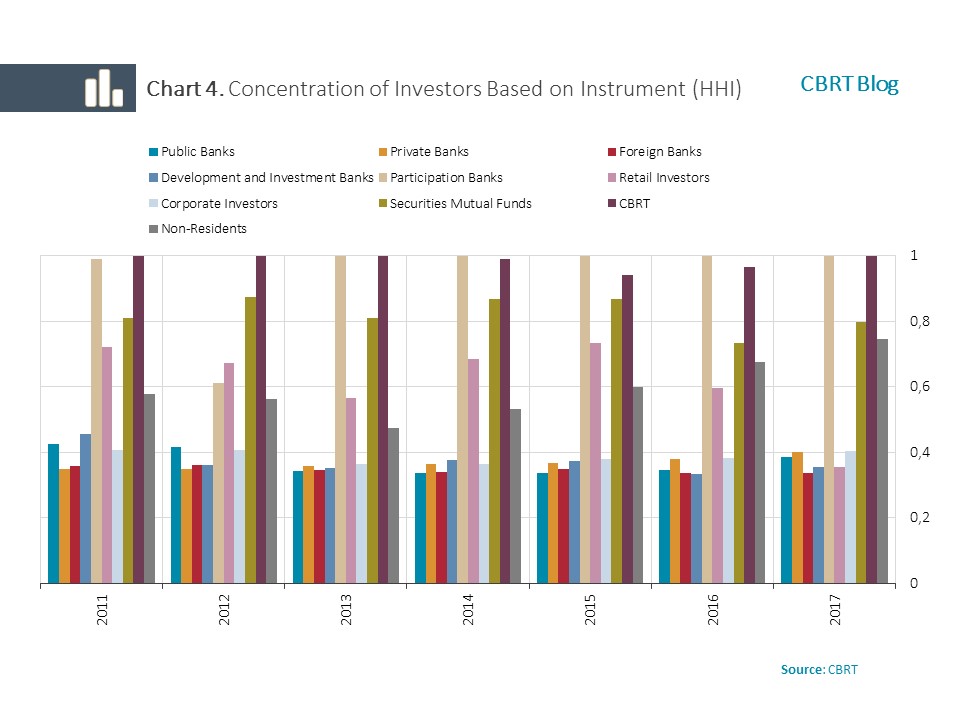

In the detailed resilience analysis for Turkey, we examine the concentration of investors based on debt instruments and vice versa. The concentration of investors by instruments is obtained via adding the squares of the shares of the instruments of each holder within the total debt stock, which measures the variety of instruments. During the 2011-2017 period, HHI values across the banking sector (excluding participation banks) were quite low, which indicates that a variety of tools was preferred by the sector (Chart 4). On the other hand, the CBRT and participation banks opted for a single instrument but the fact that their shares remained low within the total domestic debt stock holders did not hamper the resilience of the domestic debt stock.

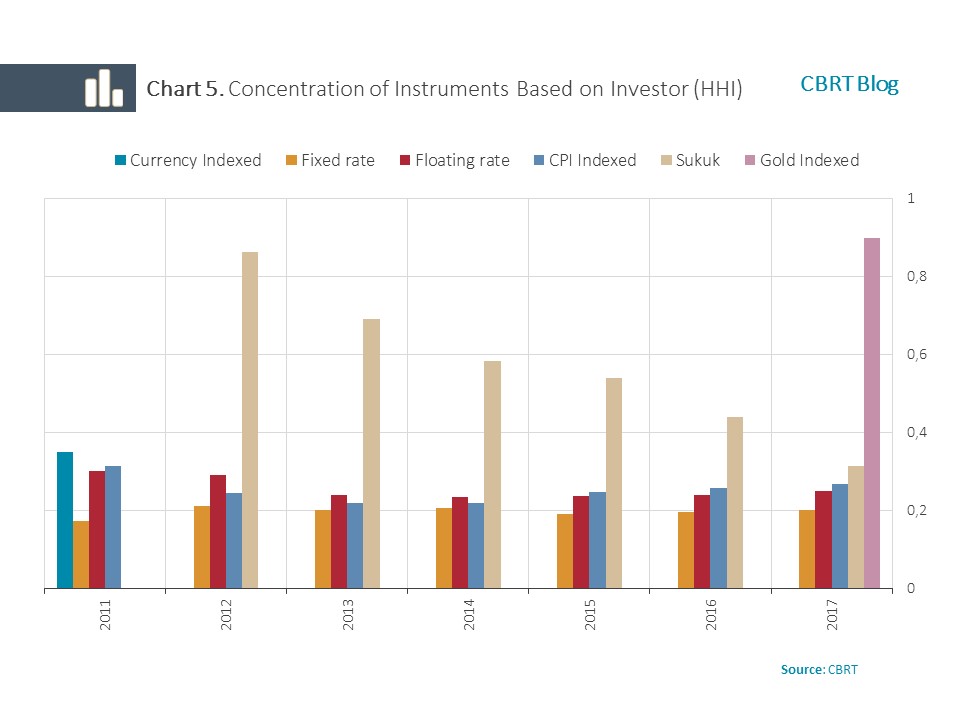

Investor-based concentration of instruments is another measure to be employed in analyzing the resilience of the domestic debt stock. An analysis of its course over years indicates a balanced composition of fixed-rate, floating-rate and CPI-indexed government bonds among investors (Chart 5).

To sum up, introduction of the data set on instrument preferences of domestic debt stock holders by the CBRT is important in terms of closing the data gap in this field and enabling comparison of the domestic debt stock structure among peer countries. Cross-country comparisons reveal that non-resident investors prefer long-term fixed-rate debt instruments. However, instrument preferences of other investors of the domestic debt stock vary across countries. Turkey has gone a long way in improving its domestic debt stock resilience recently. Reinforcing the efforts towards a broad-based private pension system is crucial to sustain this improvement. In conclusion, the analysis we have made to measure the resilience of the domestic debt stock in Turkey against possible shocks by employing this data set suggests a balanced and diversified distribution of the domestic debt stock in terms of holders and instruments.

[1] A one-to-one comparison between South Africa and Turkey is not possible on an instrument basis since South Africa has only fixed-rate and CPI-indexed bonds as domestic debt instruments.

[2] To eliminate a mismatch between investor compositions of the domestic debt stock in countries analyzed, the investor base is defined under the main categories of banks, non-residents and non-bank investors. The non-bank sector is defined for each country as follows: that which covers pension funds, insurance funds and public funds (wealth and guarantee funds) in Brazil; that which covers pension funds, insurance funds and public funds (wealth and guarantee funds) as well as other financial institutions in South Africa; that which covers institutional investors including the unemployment insurance fund representing the public funds, and securities mutual funds in Turkey.

[3] It should be noted that investors’ instrument preferences may also be influenced by the primary dealership system and similar regulations.

[4] The index has been developed to measure the degree of competitiveness in the market and is calculated by adding the squares of the shares of all domestic debt stock holders on an instrument basis and of the shares of domestic debt instruments on an investor basis. For n denoting the number of investors/debt instruments in the market and si representing the market share, .

[5] For Turkey, the domestic debt stock holder base includes the banking sector, non-residents, and the non-bank sector represented by institutional investors, retail investors, securities mutual funds and the CBRT. The unemployment insurance fund representing public funds is classified under institutional investors.

[6] Moreover, it should be noted that the ratio of domestic debt stock to GDP is approximately 28 percent in Turkey whereas this ratio is above 50 percent and 80 percent in South Africa and Brazil, respectively.

Bibliography

Arslanalp, M. S., & Tsuda, M. T. (2014). “Tracking Global Demand for Emerging Market Sovereign Debt” (No. 14-39). International Monetary Fund.

Jeanneau, S., & Pérez Verdia, C. (2005). “Reducing Financial Vulnerability: The Development of the Domestic Government Bond Market in Mexico”.

Özyer, S. İ., Tırpan, M. K., & Yılmaz, E. (2018). “Distribution of Domestic Debt Instruments by Investor Type”, CBRT Inflation Report 2018-I, Box 6.1.

Sidaoui, J., Santaella, J. A., & Pérez, J. (2012). “Banco de México and Recent Developments in Domestic Public Debt Markets”.