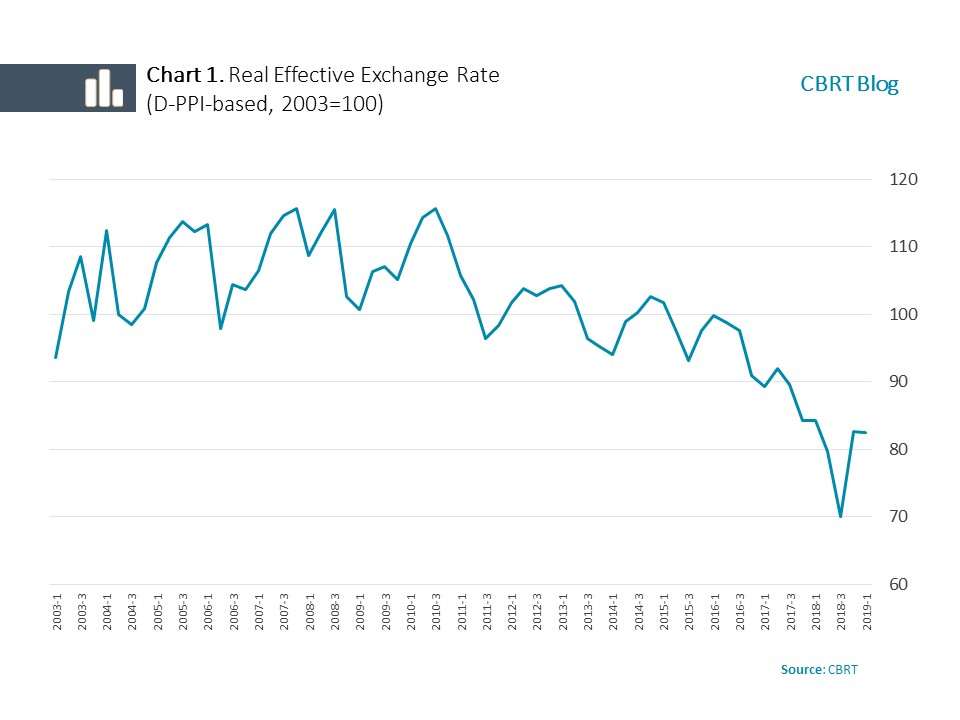

The nominal effective exchange rate is the average value of the Turkish lira weighted with bilateral trade flows, based on the basket composed of the currencies of countries that have a significant share in Turkey’s foreign trade. On the other hand, the real effective exchange rate is obtained by adjusting the nominal effective exchange rate for relative price effects. As increases (decreases) in the real effective exchange rate index would mean more expensive (cheaper) exports and cheaper (more expensive) imports relative to trade partners, they can be interpreted as competitive disadvantage (advantage) in a broader sense. Based on this interpretation, the Central Bank of the Republic of Turkey (CBRT)’s real effective exchange rate index shown in Chart 1 points to an increase in Turkey’s competitiveness in the recent period.

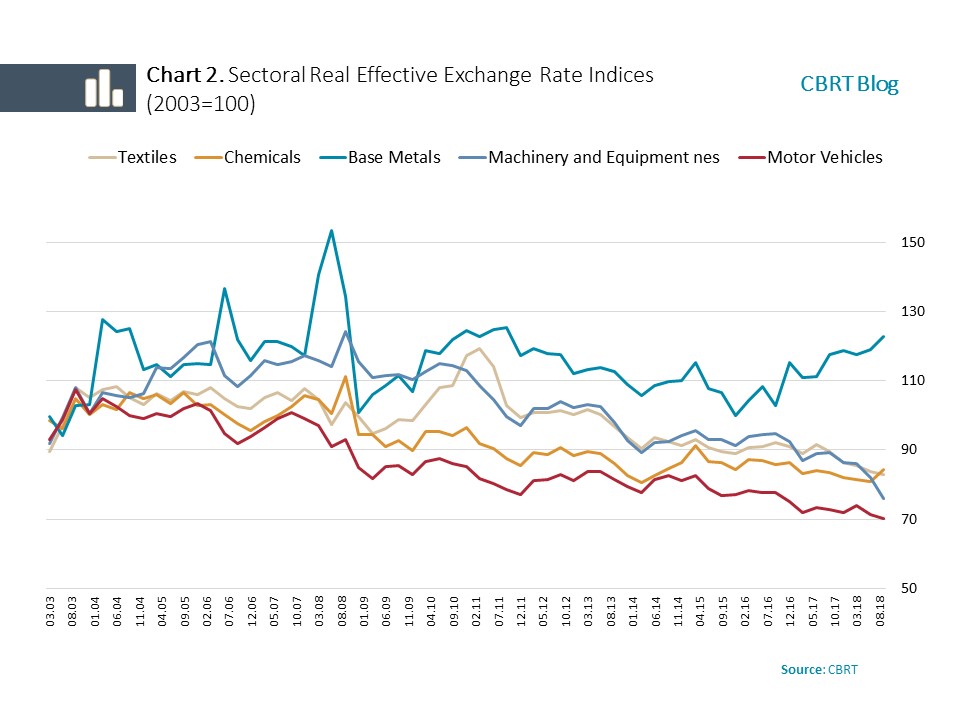

The ultimate level of exchange rate-driven competitive advantages is determined by the balance between international trade developments and productivity. In this blog post, we aim to shed light on the relation of direct sectoral competitiveness and productivity indicators with real effective exchange rate tendencies.[1] To this end, we employ the sectoral real effective exchange rate indices that the CBRT formulates on the basis of producer prices. The sectoral real effective exchange rate indicates that competitiveness developments in different segments of the economy may diverge at times (Chart 2).[2] This divergence can be instrumental in exploring the relation between the real effective exchange rate and productivity.

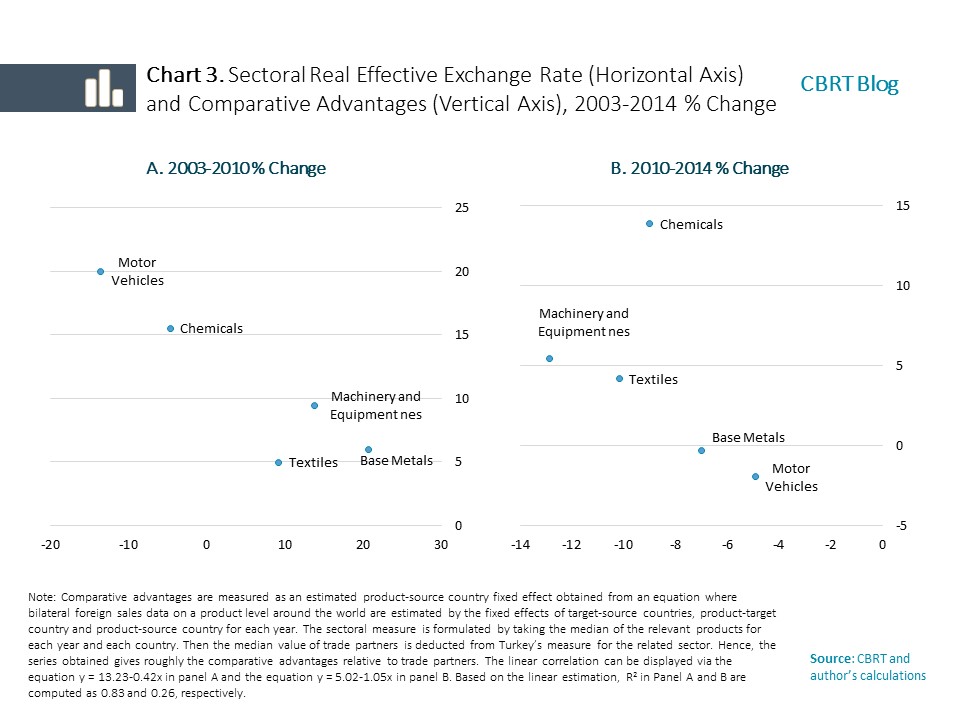

First, we focus on the relation between the sectoral real effective exchange rate and the comparative advantage variables directly calculated based on export performance. In the literature, export-based comparative advantage measures have been derived since the mid-1900s (Balassa, 1965). However, the majority of these measures fall short of measuring the “productive capacity” which is theoretically defined as a comparative advantage in cases where costs of bilateral trade between countries are asymmetric (French, 2018). Yet, via regression-based methods developed recently, it is possible to calculate theoretically consistent comparative advantages using details of data concerning product-source country-target country (Costinot et al., 2011).[3]

Chart 3 presents a comparison between the long-term growth of the sectoral real effective exchange rate and long-term growth of comparative advantage series that we have calculated in line with the theory. We examine the 2003-2010 period in which the average real effective exchange rate was relatively stable in Panel A, and the 2010-2014 period in which nominal currency depreciations were registered in Panel B. The productive capacity trend relative to foreign trade partners and the real effective exchange rate developments seem consistent with each other. As expected, the real effective exchange rate increases in both periods in the base metal sector whose productive capacity affecting foreign trade grows at a slower pace than the other sectors. On the other hand, the performance of the motor vehicles sector, which markedly increased before 2010 and has remained relatively flat since then, is confirmed by the changes both in the real effective exchange rate and comparative advantage.

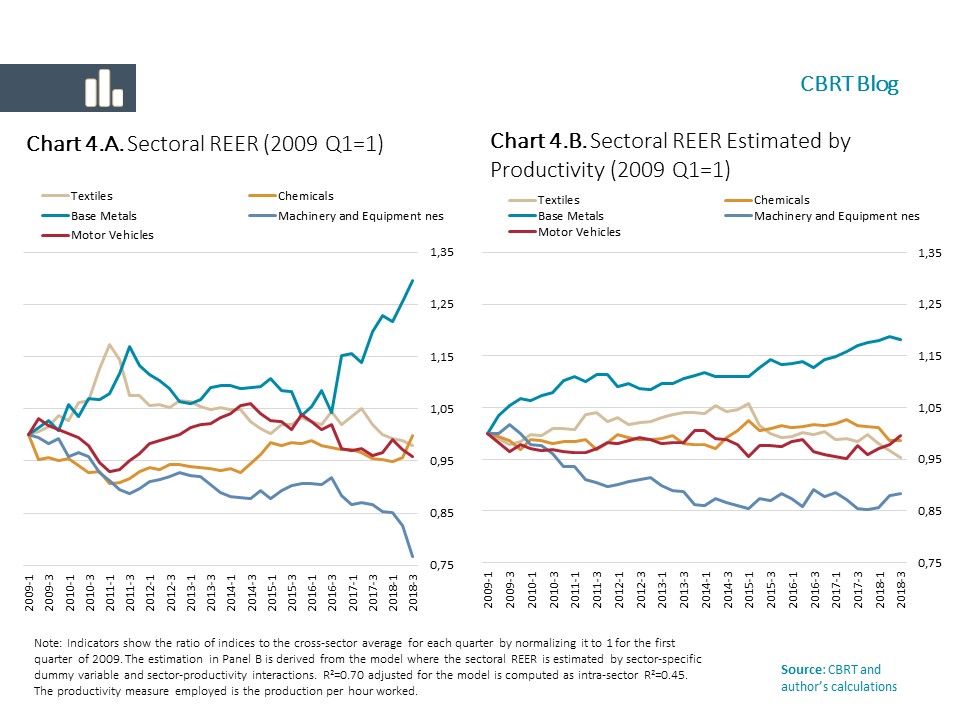

In the long term, the foreign trade-based measures roughly confirm the interpretation of sectoral real effective exchange rate in relation to competitive advantages. To be able to make higher-frequency inferences that are based on a larger number of observation points and that refer to a more recent period, quarterly productivity indicators published by the Ministry of Industry and Technology can be used. We employ a simple regression model for an estimation of sectoral real effective exchange rate series by sectoral productivity indices. Our observations regarding the role of productivity in the divergence of series since 2009 are summarized in Chart 4.[4]

Displayed on the left side of the chart, the ratios of real effective exchange rate series to their quarterly average have been normalized to 1 for the first quarter of 2009 when the productivity series began. On the right side, the same process has been applied for the sectoral real effective exchange rate estimated by productivity. As strikingly demonstrated by the chart, there is a strong relationship between productivity and sectoral real effective exchange rate indices. In other words, the competitive advantage of currency depreciations is not independent of the extent of the increase in productivity.[5]

Another point revealed by this exercise is that although productivity is the main driver of medium-term real effective exchange rate developments, factors other than productivity are also influential in short-term sectoral divergences at times. The base metal sector constitutes a recent example in this respect. In this sector, the deviation from the average has increased by 24% since the third quarter of 2016, and only 5 points of this deviation can be explained with the medium-term productivity relation. As a matter of fact, producer prices in the base metal industry sharply increased in this period compared to general producer prices. Given that this period also coincided with the easing of price competition pressures by China, competitive disadvantages that the exporters effectively suffered from may have remained below the level implied by the index in this period.[6]

In sum, the consistency of the productive capacity revealed in the form of foreign trade performance with the sectoral real effective exchange rate supports the interpretation of the decline in real effective exchange rate indices as competitive advantages. On the other hand, the strong medium-term relation between sectoral real effective exchange rate series and productivity points to the potential importance of productivity in the translation of nominal exchange rate advantages into international competitive advantages.

[1] Theoretically, relative prices of the sectors with increased relative productivity can be expected to decrease in the short term and create a competitive advantage in this way (French, 2018). This blog post does not include a method that defines the causality between real exchange rates and productivity, and thus, the inferences are interpreted based on the common movement between the two. For an analysis that summarizes the conceptual framework of the relation between the real exchange rate and productivity and that provides an economic literature review, see Özbilgin (2015).

[2] Sectoral REER for Turkey was first developed by Saygılı et al. (2012).

[3] Comparative advantages have been estimated by the equation ![]() . Here,

. Here, ![]() is the logarithm of country i’s exports of product k to country n,

is the logarithm of country i’s exports of product k to country n, ![]() is the fixed effect for the country pair of trade,

is the fixed effect for the country pair of trade, ![]() is the fixed effect for product k and country i, and

is the fixed effect for product k and country i, and ![]() is the stochastic shock on the bilateral trade of the given product. The fixed variable of product-exporting country obtained via the annual estimation of this equation by world bilateral trade data,

is the stochastic shock on the bilateral trade of the given product. The fixed variable of product-exporting country obtained via the annual estimation of this equation by world bilateral trade data, ![]() offers a theoretically consistent measure of the comparative advantage of country i regarding product k (Costinot et al., 2011; French 2018).

offers a theoretically consistent measure of the comparative advantage of country i regarding product k (Costinot et al., 2011; French 2018).

[4] The regression model employed: ![]() where

where ![]() and

and ![]() are the real effective exchange rate and productivity index of sector k in year t, respectively,

are the real effective exchange rate and productivity index of sector k in year t, respectively, ![]() is the indicator variable for sector k, and

is the indicator variable for sector k, and ![]() is the stochastic shock on the real effective exchange rate. The REER series estimated by this model has been used in Chart 4B.

is the stochastic shock on the real effective exchange rate. The REER series estimated by this model has been used in Chart 4B.

[5] The estimation yields almost the same results when the measure of productivity per worker is employed instead of the hours worked. Wages, another factor that may be related to REER changes, display relatively very close variations in the related sectors, and the estimation performance for REER changes remains low.

[6] For sectoral developments coinciding with the start of the period, see the Report of the Ferrous and Non-Ferrous Metals Assembly of Turkey (2016).

References

Balassa, Bela. "Trade liberalisation and “revealed” comparative advantage 1" The Manchester School 33, no. 2 (1965): 99-123.

Arnaud Costinot, Dave Donaldson, and Ivana Komunjer. "What goods do countries trade? A quantitative exploration of Ricardo's ideas" The Review of economic studies 79.2 (2011): 581-608.

French, Scott. "Revealed comparative advantage: What is it good for?" Journal of International Economics 106 (2017): 83-103.

Özbilgin, Hüseyin Murat. "A Review on the relationship between real exchange rate, productivity, and growth" Central Bank Review 15.2 (2015): 61.

Hülya Saygılı, Gökhan Yılmaz, Sibel Filazioğlu and Hakan Toprak, 2012. "Sektörel Reel Efektif Döviz Kurları: Türkiye Uygulaması" (Industry-Specific Real Effective Exchange Rates: Case of Turkey [in Turkish only]), CBRT Working Papers, No. 12/13

2016 Report of the Ferrous and Non-Ferrous Metals Assembly of Turkey (in Turkish), the Union of Chambers and Commodity Exchanges of Turkey, Publication No: 2017/300