The total amount of rediscount credits extended to exporter firms by the Central Bank of the Republic of Turkey (CBRT) and the number of firms making use of these credits significantly increased in 2012, with the credit amount reaching USD 15 billion by 2013. The CBRT aims to achieve two important gains via rediscount credits: to build up foreign currency reserves and to increase the amount of exports by supporting exporter firms. Rediscount credits are paid back in full and in due time, thus hitting the first goal. This blog post investigates whether the firms using rediscount credits increase their exports.

Additional costs that exporter firms face during production, logistics and marketing stages constitute the critical factors that hinder exports (Manova 2008; 2013). Therefore, in an environment where access to credits is hard and limited, firms cannot show the same export performance they do under favorable credit access conditions. In this respect, firms using rediscount credits in Turkey are expected to increase their exports.

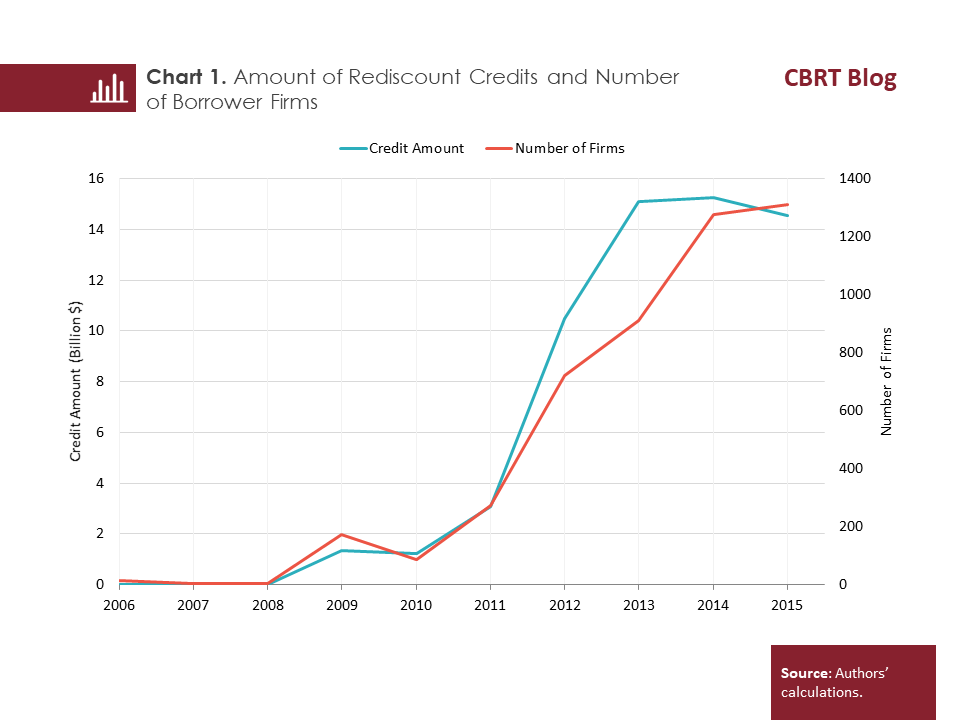

Chart 1 shows the rise in the amount of rediscount credits extended in 2012 and 2013 as well as in the number of borrower firms. The amount of rediscount credits escalated from approximately USD 3 billion in 2011 to USD 10 billion in 2012 and USD 15 billion in 2013. More than half of the rediscount credits were obtained by firms in Istanbul while a significant portion of the remaining amount was used by firms in cities with a high ratio of exports that have a Türk Eximbank (Export Credit Bank of Turkey) branch.

This study consolidates data on rediscount credits with data from the Entrepreneur Information System (EIS) of the Ministry of Science, Industry and Technology to assess the relationship between rediscount credits and firm performance. In the first stage of the empirical analysis, we identified the firms which have never obtained rediscount credits but resemble 375 firms that received rediscount credits for the first time in 2012 in terms of propensity to get rediscount credits. This identification and matching was made via the propensity score matching method using firm performance measurements and characteristics in the pre-2012 period (such as exports, total sales, domestic sales, number of employees, profitability and firm age). In this way, the selection bias originating from firms using rediscount credits was minimized. In the second stage, via a regression analysis for the period before and after 2012, firms using rediscount credits for the first time in 2012 were compared with firms matched with these firms but that have not used rediscount credits. Lastly, the generalized propensity score matching method was used to assess the effects of the amount of rediscount credits in addition to the effects of the use of rediscount credits.

The significance of the propensity score matching method is readily visible in descriptive statistics. We see that firms that obtained rediscount credits in 2012 employed a greater number of employees and had a larger amount of sales and exports in the 2009-2011 period than other exporter firms. The average number of employees is 221 in firms using rediscount credits whereas this figure is 47 in other exporter firms. Likewise, the average annual exports of firms using rediscount credits amounts to USD 13.2 million while it is USD 1.4 million in other exporter firms. On the other hand, the characteristics of firms which have not used rediscount credits as identified by the propensity score matching method were similar to those of rediscount credit-using firms in the pre-2012 period. The average number of employees and the average amount of exports of matched firms that have not used rediscount credits are 205 and USD 13 million, respectively. Statistical tests demonstrate that in terms of all the characteristics used in the method, there is a balance between matched firms and firms that have obtained rediscount credits. When evaluating the impacts of rediscount credits and devising relevant policies, it should be kept in mind that rediscount credits are received by large-scale exporter firms.

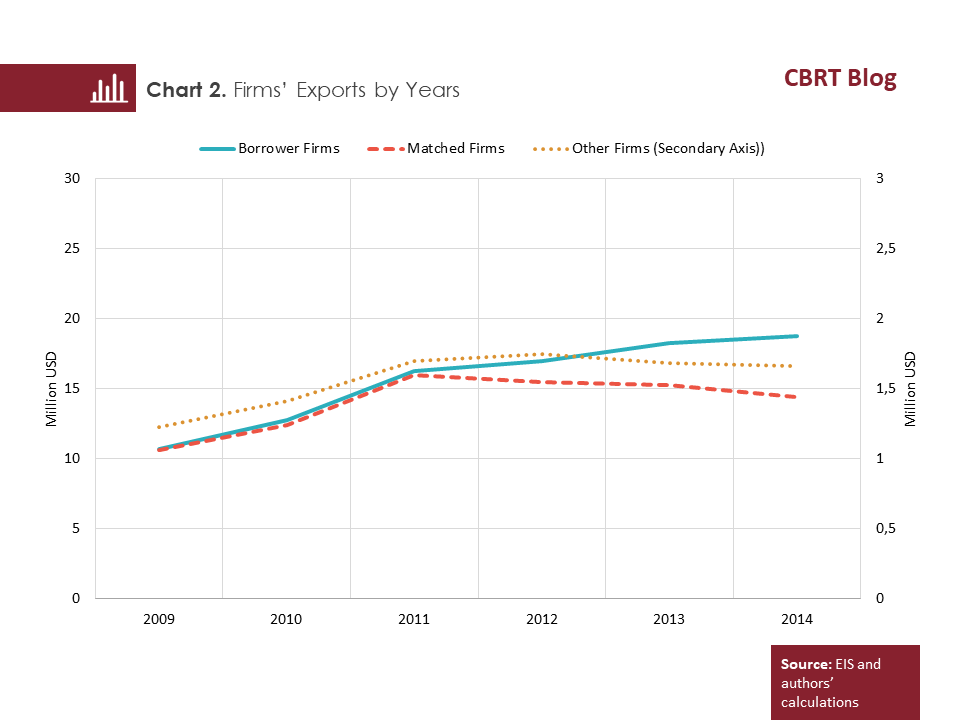

The results of the regression analysis that we conducted using the matched sample reflect the divergence in Chart 2. This analysis revealed that the exports of firms that used rediscount credits were 65% higher than the exports of matched firms in the 2012-2014 period. When we look at the relationship between the amount of rediscount credits and the amount of exports, we see that there is a statistically significant relationship between a 1-dollar rediscount credit and additional 0.21 dollars in exports in the same year. A positive but limited relationship was observed between the use of rediscount credits and the total sales. Meanwhile, we couldn’t find any significant relationship between the use of credits and the domestic sales or the amount of profits. The results support the view that firms that use rediscount credits have a higher amount of exports.

An analysis of the effect of rediscount credits based on firm size shows that obtaining rediscount credits has a disproportionately larger effect on small exporter firms. It was also found that an increase in the amount of rediscount credits does not lead to an equally positive effect on exports after a while. It should be kept in mind that certain shocks peculiar to 2012 that cannot be observed despite a matching may have urged some firms to get rediscount credits and increase their exports. In addition, we would like to emphasize that the analysis period in this study is the post-crisis period and the borrower firms are large-scale firms. Lastly, this study is not a cost-benefit analysis of rediscount credits, and the impacts of these credits on other economic factors should not be ignored. For example, it should be acknowledged that rediscount credits may create a demand for foreign currency on their repayment dates and the optimal reserve accumulation rate should also be taken into account in this process. To sum up, our findings suggest that rediscount credits support exports. Yet, it should be underlined that a number of factors should be taken into account in the design of such financing instruments and the funds should be distributed in a target-oriented and efficient way.

Bibliography

Akgündüz, Y.E., Kal, S.H. and Torun, H. (forthcoming). “Do subsidized export loans increase exports?” The World Economy.

Manova, Kalina, “Credit constraints, equity market liberalizations and international trade.”, Journal of International Economics, 2008, 76(1), 33-47.

Manova, Kalina, “Credit constraints, heterogeneous firms, and international trade.” The Review of Economic Studies, 2013, 80 (2), 711-744.