There are two factors that feed the bank liability dollarization in emerging economies: strong preference for foreign currency (FC) in domestic deposits against depreciation of local currencies, and local banks’ ability to access foreign funds only in international currencies (e.g. USD). In the related literature, this is referred as the “original sin” (Eichengreen et al. (2002)). Since the insufficiency of banks’ FC assets against FC liabilities would make the financial system vulnerable to exchange rate risks, banks’ FC open positions are restricted by certain regulations in Turkey[1]. Banks are therefore only able to lend their FC liabilities by either converting them to TL with swap operations or by directly extending loans in FC. Considering the cost and practicality difficulties of swap operations, it is easier for banks to transfer the exchange rate risk to borrowers by directly lending FC (i.e. matching FC liabilities with FC assets). Meanwhile, firms that have natural hedges (e.g. export revenues) against fluctuations in the exchange rate tend to prefer low interest rate FC loans. These tendencies, in brief, constitute the supply and demand sides of the FC credit mechanism and bring the real sector credit dollarization into an equilibrium point. What matters for the policy makers is to what extent these two trends determine the equilibrium of credit dollarization[2].

Studies, conducted with micro data for various countries, reveal that firms’ natural hedges and banks’ tendency to match assets with liabilities are influential factors in determining the real sector credit dollarization (Ongena et al. (2014) and Luca and Petrova (2008)). Although the studies on Turkey mostly support these findings, an answer to the question of “which component is more influential” has not yet been provided, given that the impact of banks’ (supply) and firms’ (demand) tendencies are analyzed separately (Alp and Yalçın (2015) and Özsoz et al. (2015)).

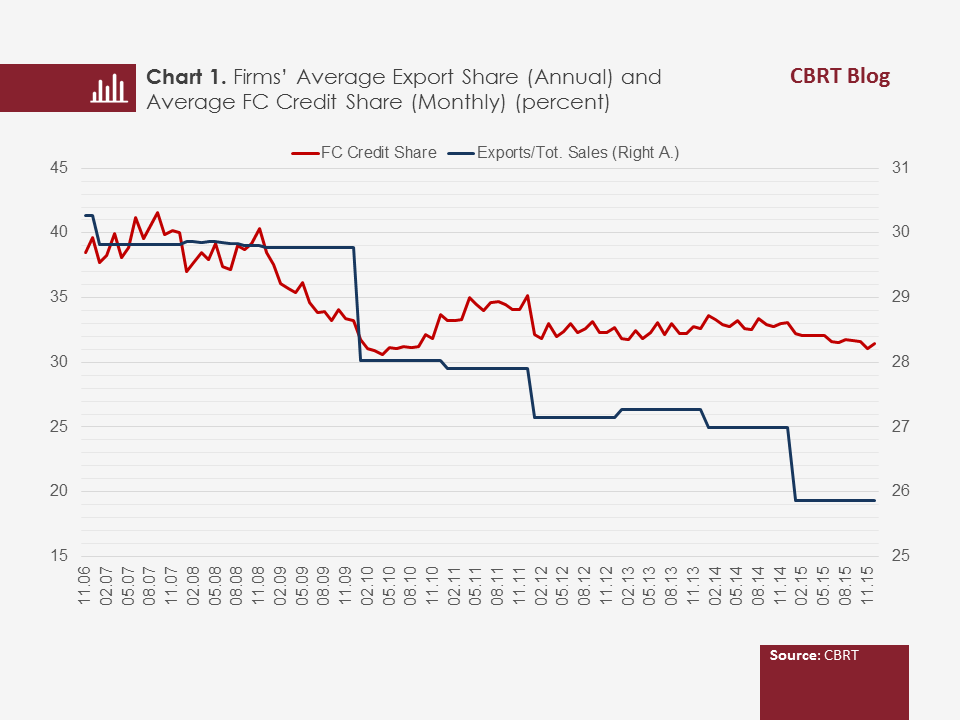

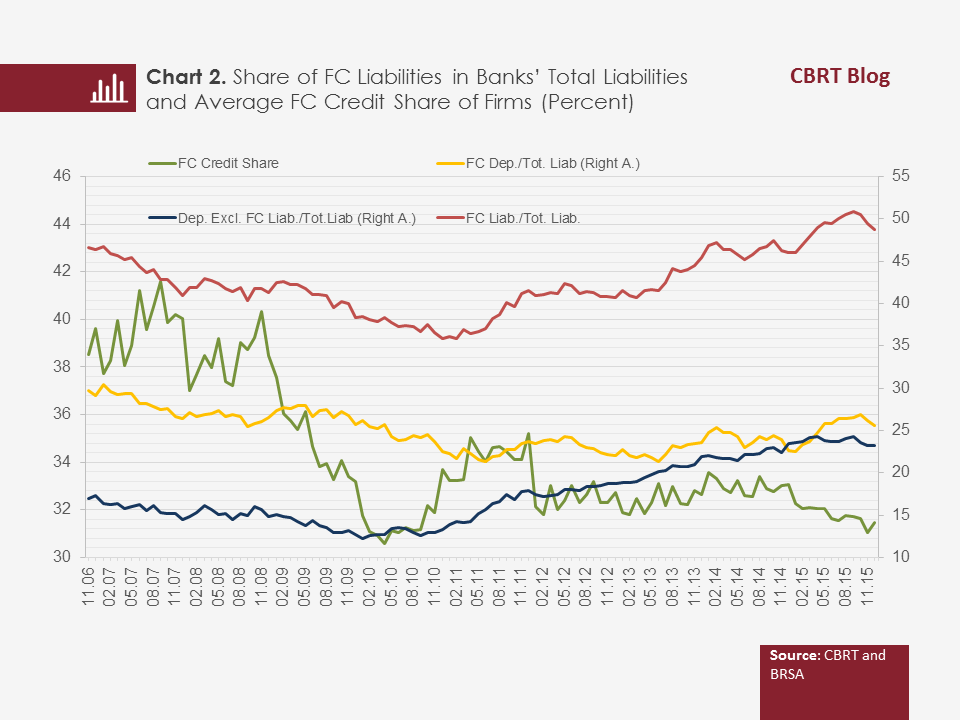

The relationship between the average firm level credit dollarization (e.g. FC credit share) and average export / total sales ratios for the sample period between 2006 and 2015 is presented in Chart 1. As per the Chart, the firms’ share of exports and FC loans show a similar downtrend. In Chart 2, the average FC liability share of the banks and the credit dollarization are presented. The positive relationship between these two variables becomes negative in the post-2013 period and the role of non-deposit FC liabilities (e.g. bonds, syndication) appears to be more prominent in this divergence. To conclude, both charts tell us that firm level credit dollarization is closely linked to both banks’ FC liability structure and firms’ natural hedges.

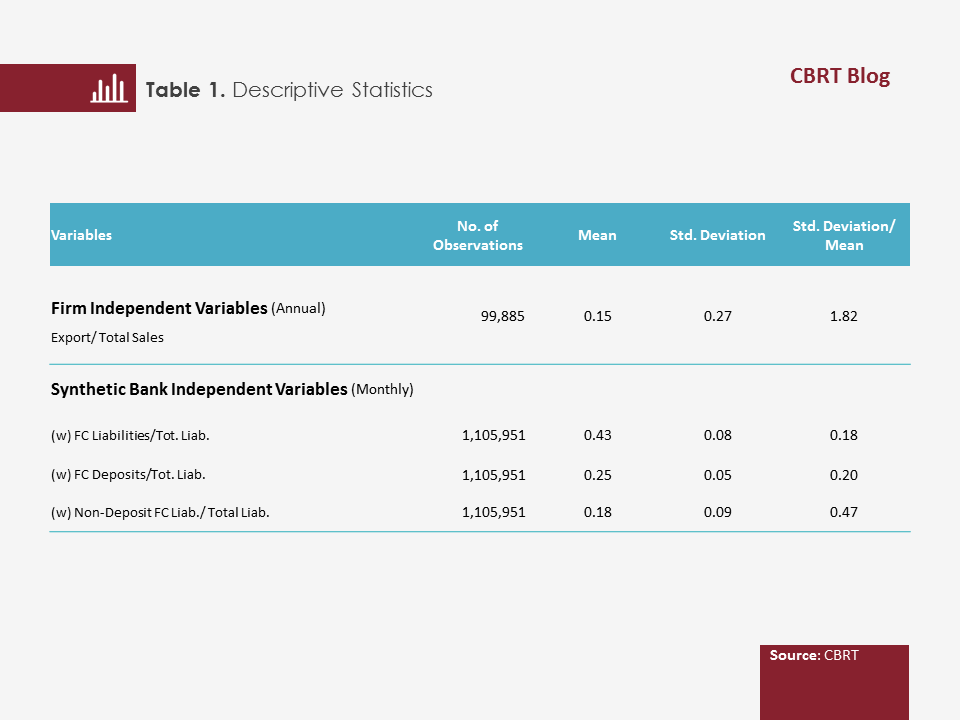

In this study, firm and bank behavior are analyzed together in an econometric analysis by using firm-bank matched credit balance data obtained from the TBB Risk Center, and firm and bank balance sheet and income statements from the CBRT and BRSA. Findings show that both firms’ propensity to rely on their natural protections and the banks' asset-liability matching tendencies drive credit dollarization. However, the bank side effect is clearly stronger. Accordingly, one standard deviation increase in exports/total sales ratio (approximately a twofold hike in average exports/sales ratio, Table 1) leads to a 1.3 percentage point rise in credit dollarization, while a similar increase in the bank FC liability ratio (20 percent expansion in average FC liability share, Table 1) corresponds to a 2 percentage point rise in credit dollarization. As for banks' FC core liabilities (FC deposits), the impact of one standard deviation increase in the share of FC deposits is 1 percentage point rise in credit dollarization. The impact of a similar increase in the share of non-deposit FC liabilities is computed to be 2.2 percentage points rise in credit dollarization.

Our analysis with Turkish data indicates that supply-side (i.e. bank) trends feed credit dollarization more strongly than demand-side (i.e. firm) trends. As a matter of fact, the impact of a rise in banks’ FC liabilities on credit dollarization is much stronger than a rise in firms’ FC income. Moreover, the impact of FC funds that the banks obtain from abroad on credit dollarization is much stronger than FC deposits. This can be attributed to the fact that these funds have longer maturities than FC deposits, which makes them preferable in FC credit financing.

[1] According to the current regulations, the net FC position (FC asset - FC liability) of banks in Turkey cannot exceed twenty percent of risk weighted assets (Official Gazette No: 26333 dated November 2006).

[2] A more detailed version of this study can be found in the Financial Stability Report May 2017, No: 24, Special Topic IV.3. Drivers of Credit Dollarization.

References:

Eichengreen, B., Hausmann, R. and Panizza, U. (2002). Original Sin: The Pain, the Mystery and the Road to Redemption. Paper prepared for the conference Currency and Maturity Matchmaking: Redeeming Debt from Original Sin. Inter-American Development Bank, Washington, D.C., 21-22 November 2002.

Alp, B. and Yalçın, C (2015). Türkiye’de Şirketlerin Borç Dolarizasyonu ve Büyüme Performansı. (Liability Dollarization and Growth Performance of Non-Financial Firms in Turkey- available in Turkish only) Working Paper, CBRT 15/01.

Luca, A. and Petrova, I. (2008). What drives credit dollarization in transition economies? Journal of Banking & Finance, Elsevier, 32(5), 858-869.

Ongena, S., Schindele, I. and Vonnák, D. (2014). In lands of foreign currency credit, bank lending channels run through? The effects of monetary policy at home and abroad on the currency denomination of the supply of credit, CFS Working Paper Series 474, Center for Financial Studies (CFS).

Özsoz, E., Rengifo, E. W. and Kutan, A. (2015). Foreign Currency Lending and Banking System Stability: New Evidence from Turkey, Central Bank Review, 15, No:2.