To ensure publication of data on external liabilities under one roof with a holistic approach as part of coordinated efforts between the Republic of Türkiye Ministry of Treasury and Finance (MoTF) and the Central Bank of the Republic of Türkiye (CBRT), the CBRT started publishing the External Debt Statistics of Türkiye as of March 12, 2026, which were previously released by the MoTF. Additionally, as part of the efforts to apply the residency principle in Balance of Payments Statistics, the CBRT also began employing new microdata sources to compile securities interest expenditures. In this blog post, we address the methodological grounds and the implications of the revisions in Türkiye’s external debt and balance of payments statistics.

Methodological Change in External Debt Statistics and Its Implications

The External Debt Statistics Guide of the International Monetary Fund (IMF) arranges the methodological standards for External Debt Statistics. Accordingly, the residency of creditors of debt securities should be identified according to the resident country of securities holders, not the issuing country. For example, if non-residents are the buyers of a domestic debt security issued by the General Government, the related statistics should be recorded as external debt, not as domestic debt. Likewise, if residents are the buyers of a debt security issued abroad, this security is not classified as external debt but as domestic debt.

In the former version of External Debt Statistics of Türkiye by the MoTF, the classification of debt instruments was based on the issuing country, with domestic debt instruments monitored under domestic debt and all external debt instruments monitored under external debt. The methodological change has introduced a classification based on the residency of securities holders rather than the issuing country, and revised the valuation using market values instead of nominal amounts. Thus, External Debt Statistics have also become fully harmonized with the International Investment Position (IIP) Statistics that already comply with the same standard.

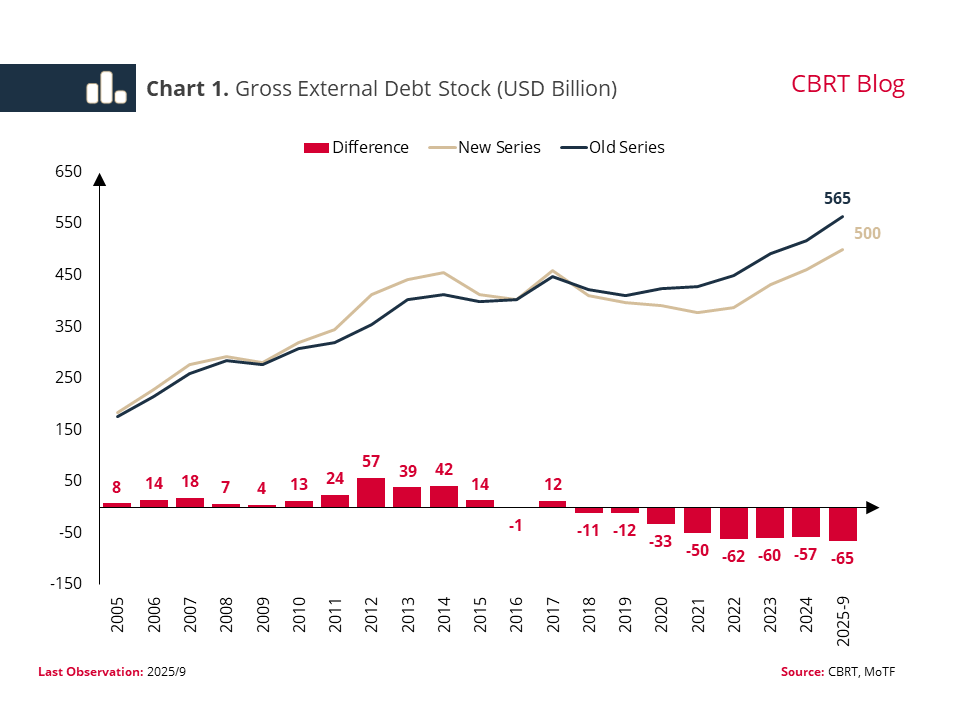

Using the new methodology, the CBRT revised the External Debt Statistics retrospectively until 2005. As of the third quarter of 2025, this revision brought about a decline of approximately USD 65 billion in the external debt stock, while, at the same time, leading to a decrease in the ratio of external debt to gross domestic product, from 36.7% to 32.5%. When compared with the external debt series compiled based on the former method, the methodological alignment drove the external debt stock up for the 2005-2016 period, while it pulled the same down for the post-2017 period (Chart 1).

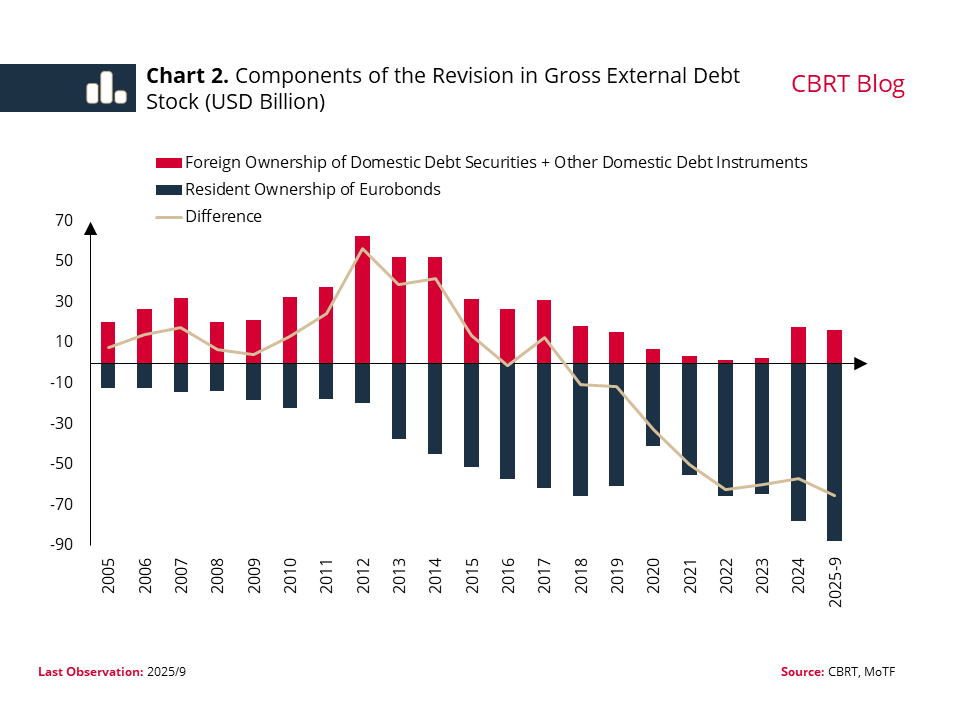

The reason for the old external debt series remaining below the new series prior to 2017 was the high rate of foreign ownership of domestic debt securities in the respective period. After 2017, though, the new series remained below the old series due to a lower rate of foreign ownership regarding domestic debt securities and higher amounts of external debt securities held by residents (Chart 2).

Methodological Change in Calculating Interest Expenditures of Portfolio Investments Under Balance of Payments Primary Income, and Its Implications

To incorporate the residency principle in debt securities into Balance of Payments Statistics, the CBRT has also changed the data sources for compilation of interest expenditures arising from securities liabilities that constitute the “Debit” item under Primary Income.

As part of the integration of administrative records-based microdata into statistical data compilation processes, the CBRT switched to a direct securities-based calculation method for interest paid on debt instruments previously tracked on an aggregated basis through banks. This new method brings together ownership information for all securities and the data on interest paid on domestic issuances by the General Government provided from CBRT; along with information on the interest type, interest rate, and coupon frequency of securities obtained from the Central Securities Depository of Türkiye (MKK), based on their ISIN codes. Thus, interest payments made to non-residents are more precisely broken down for each security and by period, enhancing the quality of the data.

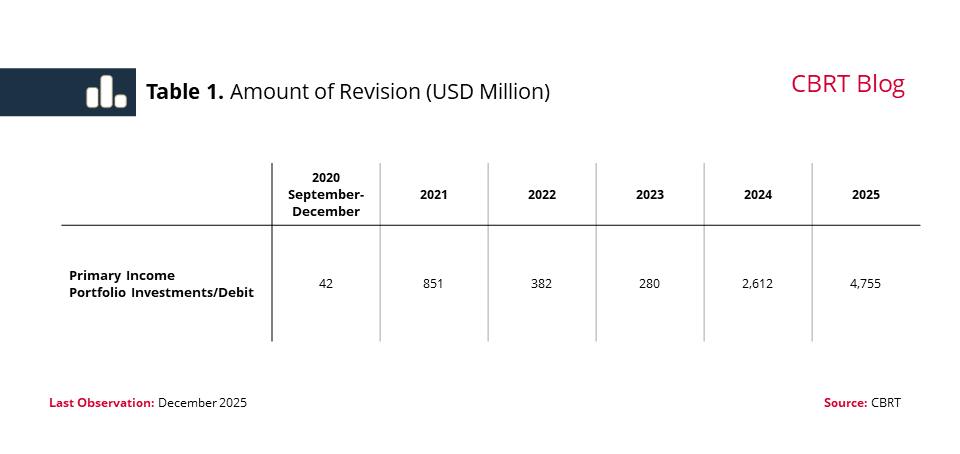

This methodological change resulted in an upward revision of USD 8,922 million to the “Portfolio Investments / Debit” item under the Balance of Payments Statistics Primary Income, starting from September 2020 (Table 1). In parallel, the CBRT retrospectively revised the Current Account Balance and the Net Errors and Omissions item at the same amount for this period. Accordingly, the current account deficit-to-GDP ratio stood at 1.9% in 2025.

To conclude, revisions to External Debt and Balance of Payments statistics yield comparable data consistent with international methodology and eliminate discrepancies in statistics related to external liabilities. Additionally, the new microdata-driven approach used in calculating interest expenditures arising from portfolio investments in the balance of payments enables the cost of Türkiye's external liabilities to be calculated in full compliance with international standards.