Use of derivatives is nowadays quite popular in financial markets as a result of the increased variety of financial instruments entailed by financial needs and innovations. Derivatives can be used either in search of a return or to yield an arbitrage profit, yet they can be resorted to for hedging purposes. Derivatives are not new to the corporate sector firms (firms) operating in Turkey, either. Firms also are expected to use derivatives for hedging purposes. A considerable portion of derivative transactions conducted by firms is composed of over-the-counter (OTC) transactions. OTC transactions are mainly conducted with banks.

This post examines the evolution of derivative transactions conducted by firms with resident banks. What is more, pricings in transactions, in which the corporate sector is a party, are central to understanding the costs incurred. Therefore, in addition to derivative transactions, the TL interest rates implied by forward rates are calculated by analyzing data on a transaction basis.

Derivative Position of the Corporate Sector

This part of the analysis presents evaluations regarding active (unexpired) transactions as of 25 January 2018. According to the CBRT data, 2,380 firms had derivative positions involving resident banks as counterparties by 25 January. Whereas, calculations from January 2014 onwards state that a total of 9,416 firms have been involved in at least one derivative transaction with banks. It is therefore apparent that derivatives are intensively used by firms and the financial sector.

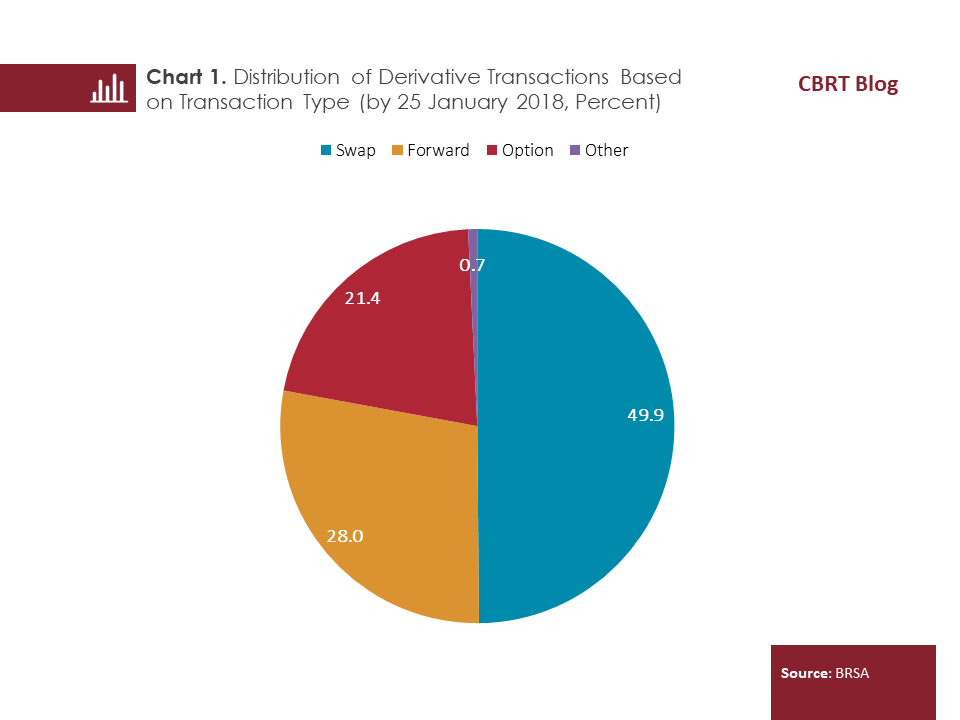

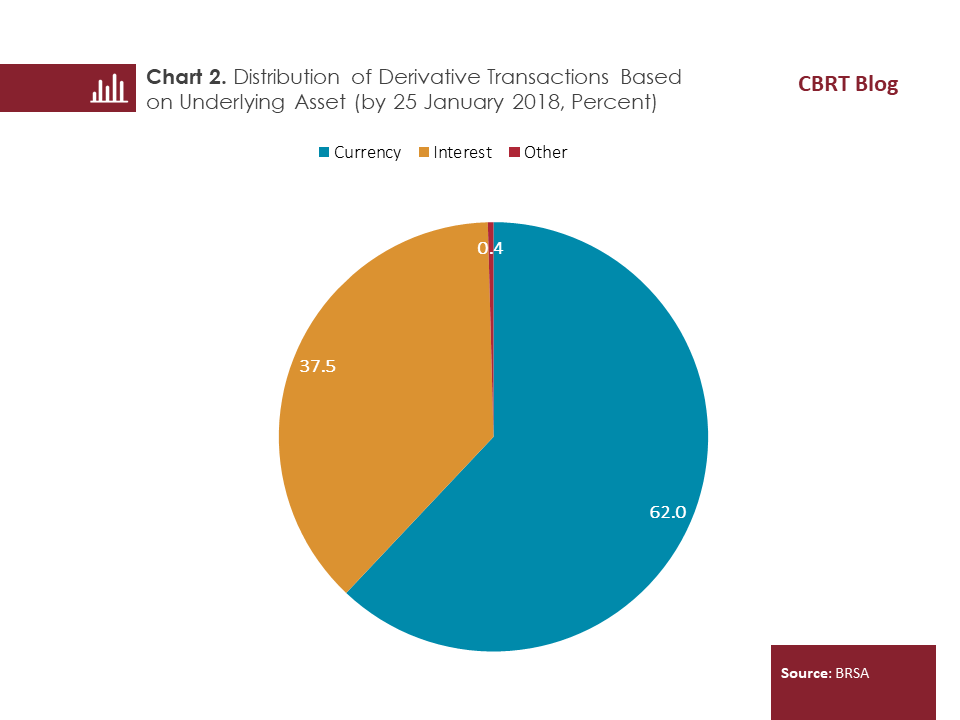

The nominal amount of the transactions conducted by firms with resident banks was approximately 231 billion TL as of 25 January. Firms predominantly conducted swap transactions (Chart 1), followed by forwards and options. An analysis of derivatives by underlying assets suggests that a significant bulk of transactions was composed of transactions based on currency. Considering assets of firms with FX short and long positions, it is not surprising to see that currency transactions account for most of the derivative transactions. Interest-driven transactions are also expected to have a significant share in firms’ derivative transactions due to the fact that a significant portion of corporate loans is composed of floating rate loans. As a matter of fact, interest-based derivatives are also used intensively by firms for an effective management of interest rate risks (Chart 2).

TL Interest Rates Implied by Forwards

This part presents a calculation of the interest rate implied for forwards that include foreign exchange purchases of the corporate sector. Although forward rates are known by parties at the transaction date, they may not be a direct representative of costs. So, calculation of implied interest rates allows for a more effective comparison in tracking the cost of forwards.

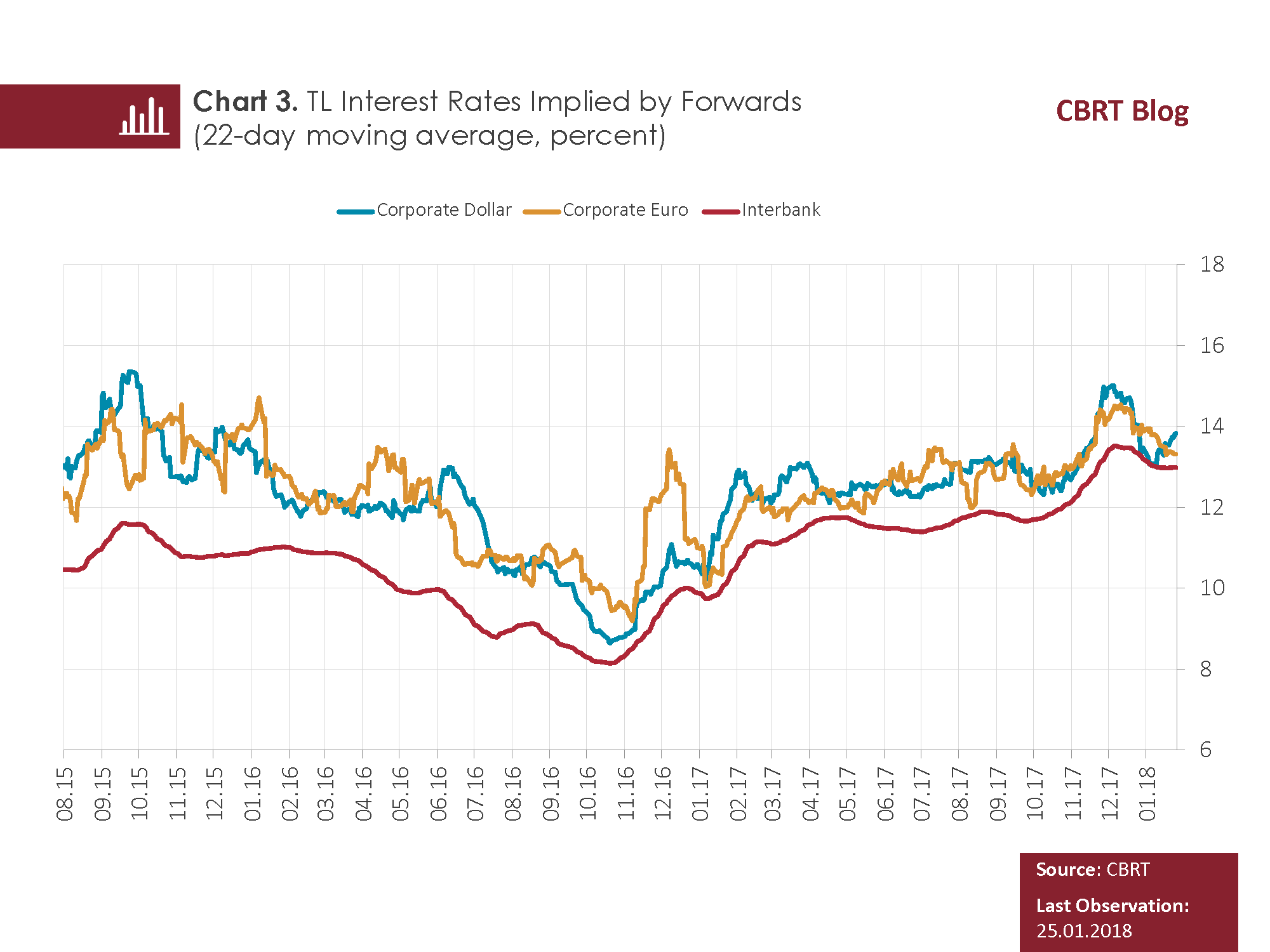

It is already stated that forwards have a significant share in firms’ total derivative transactions. Therefore, the cost of forwards is essential in managing the exchange rate risk. Through Bloomberg portal, we can keep a track of TL interest rates implied by forwards executed on interbank markets. Meanwhile, TL interest rates implied by forwards of the corporate sector can be expected to deviate from the interest rates on transactions executed on the interbank money market.

The forward rate driven by forwards in TL and FX is computed by using the following formula[1].

F0 = S0 x e (TL interest rate-FX interest rate)

In this formula, F0 represents forward rate, S0 spot rate, and e (TL rate-FX rate) represents discount factor.

When we draw the TL interest rate from the equation, the formula is shaped as follows:

TL interest rate = [ln (F0/S0)]+ FX interest rate

This computation is based on uncovered interest rate parity. The calculated exchange rate represents the rate that equalizes the return in the case of an investment in a TL or FX-based instrument during the same period. The Central Bank’s database contains spot prices and forward prices of forward transactions conducted by the corporate sector. Computations are based on these data. In this study, forward FX purchase transactions of the corporate sector were taken into consideration. The computed TL interest rate represents the TL interest rate implied by the current forwards operations.

Data of approximately 112 thousand transactions were used in interest rate calculations. As transactions with maturities of less than 10 days distorted the analysis, they were excluded from the sampling[2]. The evolution of TL interest rates implied by forwards is given in Chart 3. As interests on transactions that are conducted on certain days fluctuate significantly, the levels were considered as averages of 22 working days. Accordingly, the implied TL interest rates derived from calculations are largely consistent with the interest movements implied by interbank dollar-denominated forwards with 6-month-maturities obtained from Bloomberg[3]. As expected almost in all periods, the TL interest rates implied by corporate sector’s forwards are above those implied by interbank transactions. The banking sector applied a certain margin to forwards transactions it conducted with the corporate sector. On 25 January, while the implied interest rate on interbank forwards was 13 percent, the TL interest rates implied by dollar and euro-denominated forwards of the corporate sector were 13.8 percent and 13.3 percent, respectively. Briefly, the interest rates implied by corporate sector forwards did not show a notable divergence from the interest rate implied by transactions executed in interbank markets.

Conclusion

In conclusion, derivatives are not a new concept for our firms. Firms are already actively using derivative transactions, primarily swap, forwards and options. Moreover, the cost of forwards used by the corporate sector in managing the exchange rate risk is akin to the costs of banks.

[1] Although various methods exist for calculating forward rates, this study used the continuous compounding method.

[2] Implied interest rates of a specific date were calculated by using the data pertaining to transactions conducted on the specified date. The average maturity was also considered in calculations of TL interest rates, whereas 6-month Libor and Euribor interest rates were used for FX interest rates. The average interest rate on a specific date was calculated by weighing with the amounts of forwards conducted on the specified date. Then, the interest rates calculated for transactions were annualized by multiplying by 365/maturity.

[3] The maturity of firms’ forward foreign exchange purchases varies from 6 to 10 months during the relevant period. Hence, the implied interest rate is compared with TL interest rates on 6-month maturities implied on the interbank forwards market.