Portfolio flows to emerging market economies (EMEs) have accelerated following the expansionary liquidity policies of advanced economies after the global financial crisis. The long-lasting low interest rate environment of advanced economies drove investors towards higher-yielding EME assets. The presence of global funds can boost investment and growth in emerging economies and help develop domestic financial markets. Yet, at the same time, the behavior of global fund flows may increase the volatility in asset markets, amplifying the boom and bust periods through the balance sheet channel. Indeed, following the “taper tantrum”[1] on 22 May 2013, there were sharp withdrawals from EME bond and equity markets, which led to a drastic depreciation in their currencies, an increase in the EME firms’ risk of financing. Thus, understanding the investor behavior during these large portfolio shifts is crucial, given the increasing trend toward bond market financing by the corporate sector in EMEs.

As asset management funds increase their presence in small and relatively less liquid EMEs, fragilities associated with these markets become more evident. The value of funds managed by the largest 500 asset management companies amounts to a total of approximately 70 trillion dollars. A shift in only one percent of these assets means an additional portfolio movement of 700 billion dollars. This amount is approximately three times larger than the total portfolio amount that flowed out of EMEs at the onset of the global financial crisis in 2008! Therefore, considering the recent fluctuations in portfolio flows, it is critically important to monitor and understand the changing behavior of global portfolio investors towards EMEs.

Stylized facts regarding the changing investor behavior...

The volatile and procyclical nature of capital flows, coupled with their massive volume, has always been a concern for policymakers. The literature points out that different types of capital flows display different behavior, thereby creating different concerns for policymakers. It is conventionally assumed that within the portfolio flows, bonds tend to introduce more fragility compared to equities. Substantial depreciations in exchange rates may lead to adverse balance sheet effects. Within the debt liabilities, a distinction between foreign and local currency instruments is relevant as well. Greater ratios of foreign currency debt to total debt, depending on the accountability of a country’s reserves and policies, are usually associated with increased prospects of a sudden stop. Although the introduction of local currency instruments over the last decade has led to a decreasing share of foreign currency debt, almost one third of the EME corporate bonds are still denominated in foreign currency, thereby keeping the severity of the issue on agenda. Duration of bonds is another critical aspect to be taken into account. Short-term debt instruments are, in general, accepted riskier than long-term ones, and the long-term instruments are, in principle, more compatible with the fundamentals of the economy.

What we have mentioned so far relates to macro aspects of investor behaviors. A micro analysis of portfolio flows, on the other hand, highlights the “type of investor” as an important sub-division. Among non-resident investors, institutional investors may pursue different strategies than retail investors and this may result in different responses to local and global shocks. For instance, the rising trend of benchmarking among institutional investors may increase the degree of exposure to exogenous shocks, as the cross-country co-movement of asset prices increases. In addition, non-residents are more likely to react to global shocks whereas residents are more likely to react to local shocks. In this context, recent studies emphasize the balancing role of local investors in economies that are financially integrated with global markets.

What do the data say about the changing investor behavior?

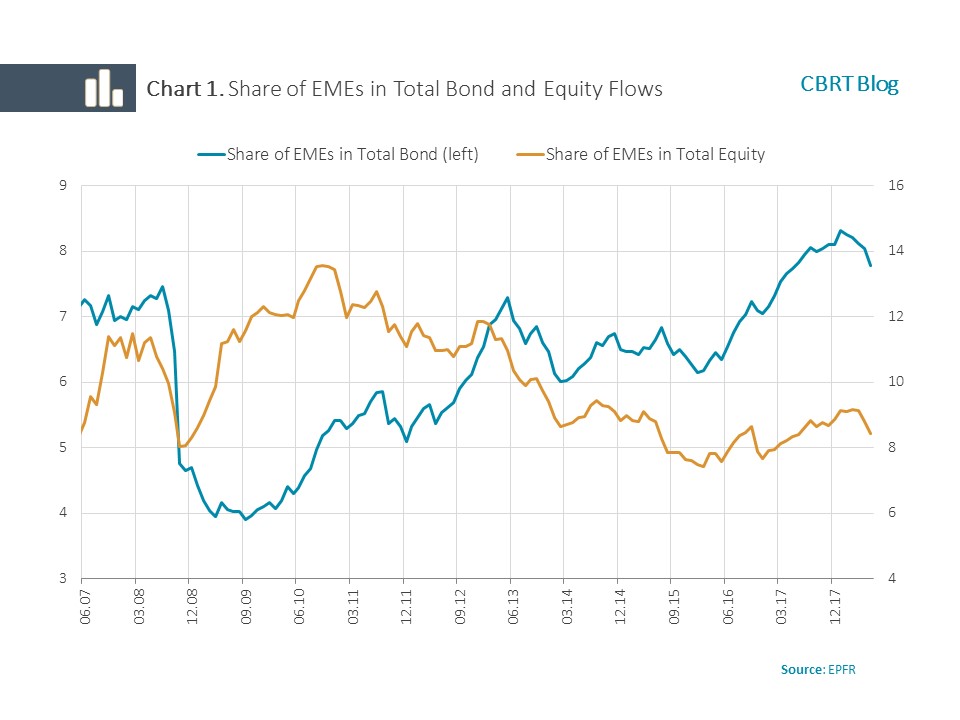

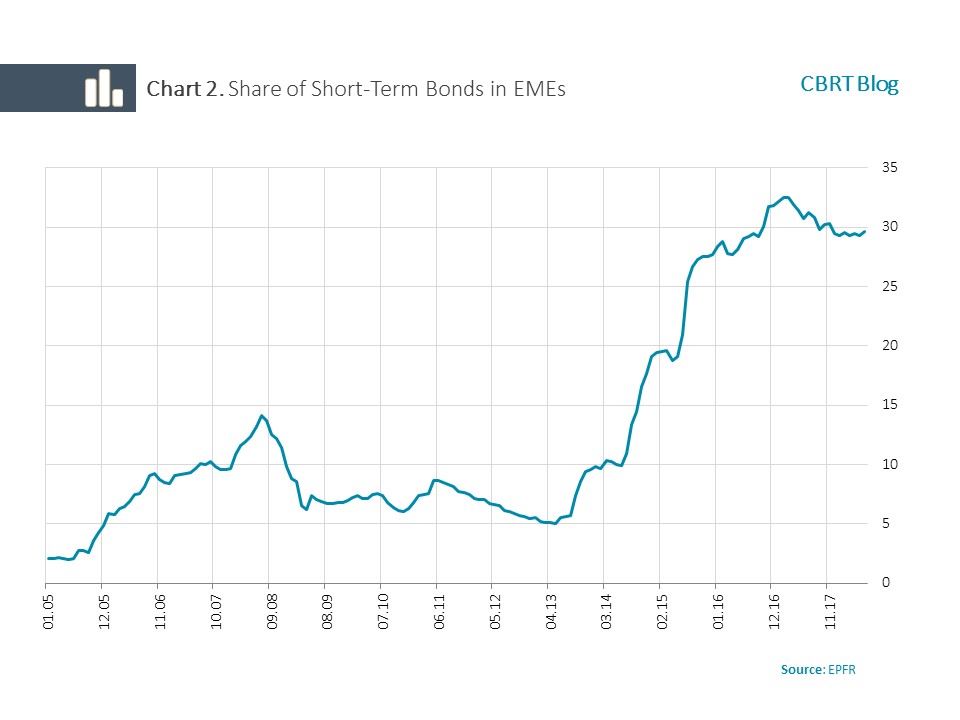

The composition of portfolio flows towards EMEs has altered dramatically since the “taper tantrum”. The Emerging Portfolio Fund Research (EPFR) data reveal an outstanding shift of portfolio flows from equities towards bonds. Global portfolio investors have increased their presence in EME bond market over the past decade and the share of EME bonds in global bond funds has doubled since the global financial crisis (Chart 1). Moreover, the share of short-term bonds in total EME bond flows has increased significantly since the “taper tantrum” (Chart 2).

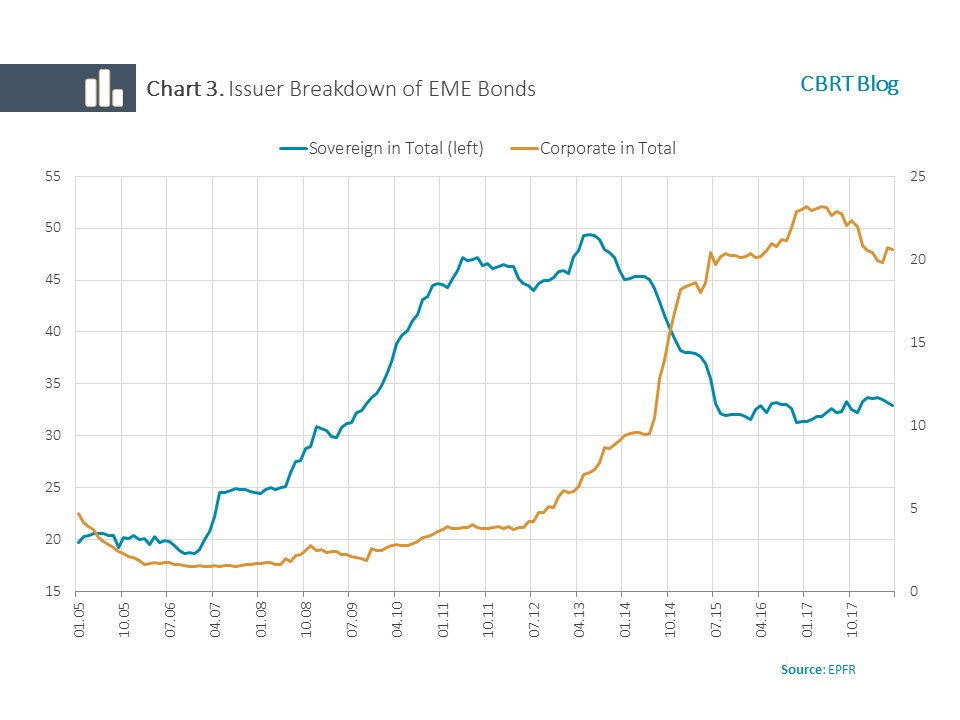

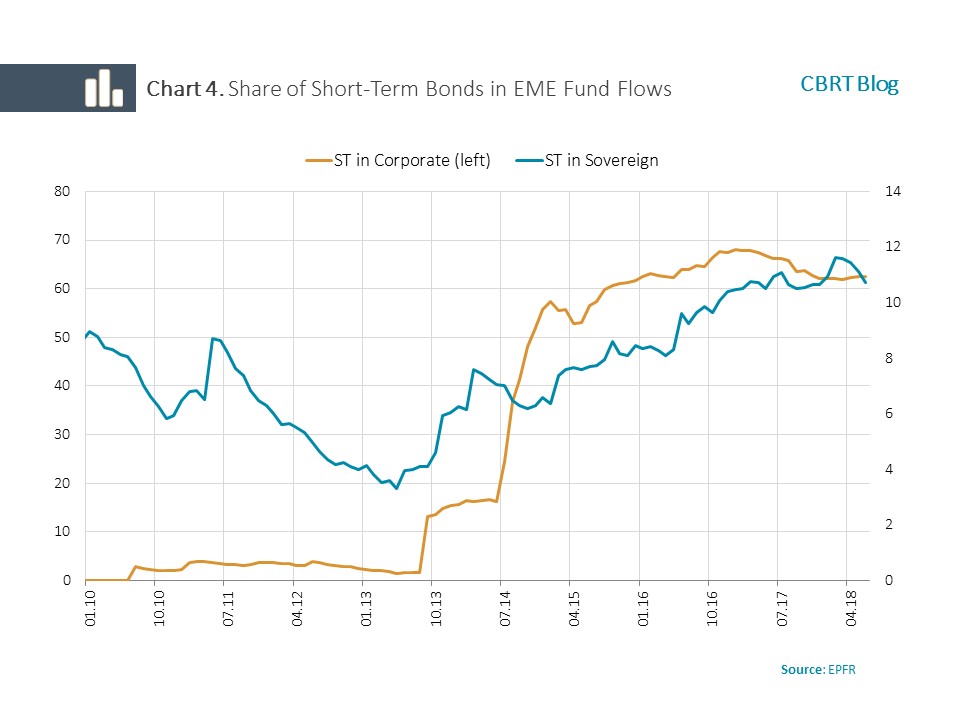

There has also been a notable rotation from government bonds to corporate bonds after the taper tantrum (Chart 3). In fact, the share of corporate sector bonds in total EME bonds increased to 20 percent as of June 2018 from 2.5 percent at end-2009. At the same time, the duration of bonds shifted towards the short-term (Chart 4).

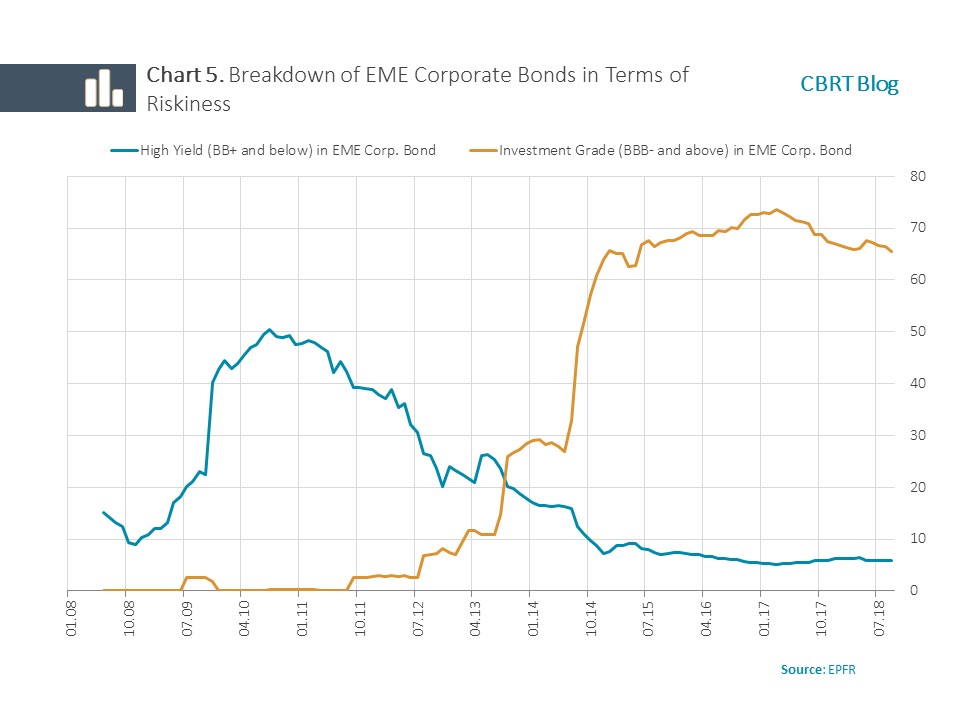

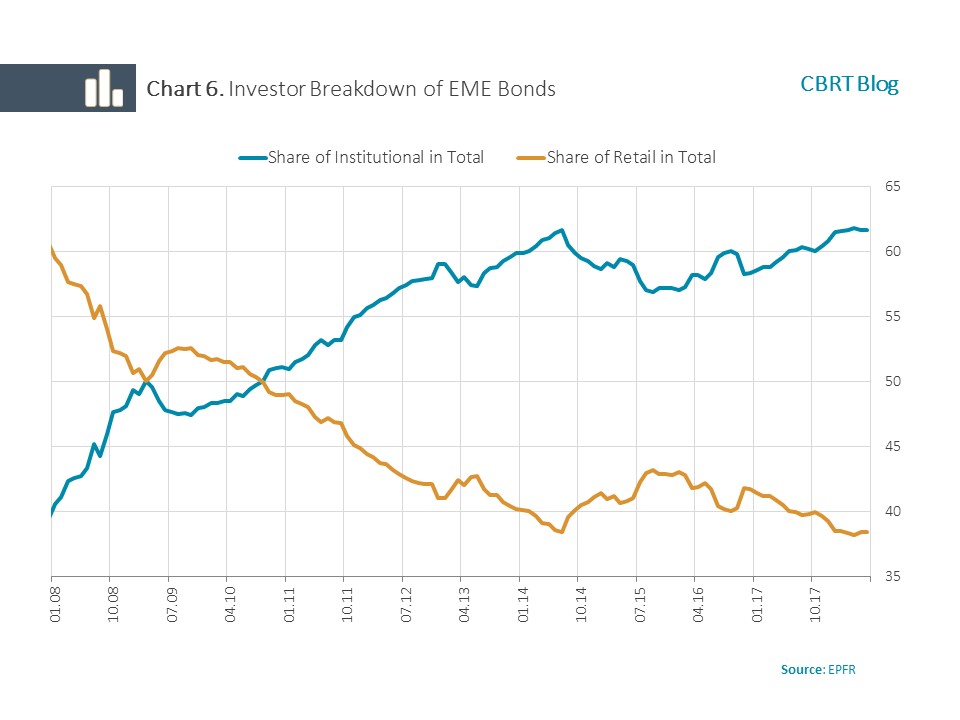

Although investors have increased their exposure to corporate bonds in EMEs, asset allocation has shifted to safer securities (Chart 5). The share of corporate bonds with higher investment grade surged from 0.5 percent in 2010 to 70 percent by June 2018, with the most of this surge seen after 2013. In this respect, following the “taper tantrum”, the motivation of investors significantly shifted away from the “high yield” motivation of the post-crisis period. Correspondingly, it is safe to say that country-specific factors have been more decisive in investor behavior after the second half of 2013. Finally, the investor type breakdown of EME assets shows a gradual increase in the share of institutional investors, whereas the share of retail investors shows a steady downward trend (Chart 6).

In sum, there has been a dramatic change in the composition of portfolio flows to EMEs that has increasingly shifted from long to shorter term, from sovereign to corporates, and from equities to bonds. In addition, institutional investors tend to have a stronger appetite for EME assets, resulting in a declining share of retail investors. With the retrenchment of global liquidity, these changes may imply higher sensitivity to global shocks, posing significant challenges for emerging economies. In these circumstances, macroprudential and structural regulations strengthening the resilience to exogenous shocks become more of an issue. In view of the increased corporate sector debt in emerging economies in particular, reducing the exchange rate mismatches and effectively monitoring the leverage and exchange rate risk of large corporates are critical to containing the effects of the balance sheet channel on domestic markets.

[1] In this speech, Ben Bernanke, the then-Chairman of the Fed, signaled for the first time that the quantitative expansion program would be terminated gradually. It is called “taper tantrum” due to the impact it had on EMEs.