The money supply refers to aggregates that show the amount of money circulating in an economy as well as certain financial instruments under specific classifications based on their degree of liquidity. These aggregates are classified in Turkey as narrow (M1), intermediate (M2) and broad (M3) money supply as shown in the table below, and they are announced on a weekly basis in period-end stock values. As foreign currency (FX) liquid assets are a close substitute for analogous Turkish lira (TL) assets for money holders, FX aggregates are also included in the money supply.

In the calculation of money supply, TL items are valued based on market value and FX items based on the relevant period-end exchange rate. Therefore, even though all items under the definition of money supply remain constant by definition, a change in exchange rates may affect the money supply. That the changes in exchange rates affect the money supply through the purchasing power of savers is an economically significant fact to consider. However, particularly in times of high volatility in exchange rates, the exchange rate effect causes the volatility in money supply to appear higher than it actually is. In this respect, simultaneously monitoring exchange rate-adjusted and non-exchange-rate-adjusted money supplies in economies with a high share of FX deposits in money supply may be helpful for a sounder interpretation of underlying trends.

The most recent data reveals that the share of TL deposits in M3 is 48% while that of FX deposits and other items is 43% and 9%, respectively. These ratios demonstrate that exchange rate fluctuations have a significant role in the change in money supply in Turkey. Therefore, besides the weekly money supply data it publishes on the EVDS[1] , the CBRT has also decided to publish the “index of notional amounts” that can be used in the calculation of exchange rate-adjusted growth rates.

In this blog post, we describe how we calculate the exchange rate effect for FX deposits under the definition of money supply announced on a weekly basis, and present exchange rate-adjusted growth rates of money supply. Exchange rate-adjusted growth rates of money supply are calculated in two steps: calculation of the exchange rate effect and formulation of the index of notional amounts.

Step 1: Decomposition of the exchange rate effect

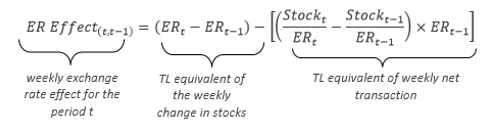

In this step, the change from one period to another is decomposed as “net change” (the change to be seen in the stock if there were no exchange rate movement) and “exchange rate-driven change”. The calculation method varies depending on the method of reporting the item to be adjusted for the exchange rate. That is to say, under weekly money and banking statistics, banks report US dollar and euro deposits in their original currency amounts, other FX deposits in their USD equivalent, and precious metal deposit accounts in their TL equivalent.

The exchange rate effect for deposits reported in original currency (in dollar and euro) is calculated as follows:

In this equation, the variables ERt and ERt-1 denote the exchange rate for the related currency in week t and week t-1, respectively. For example, the CBRT’s euro buying rates in week t and week t-1 are used for euro deposits.

In their weekly reports, banks also classify deposits denominated in currencies other than the dollar and the euro as “other” and report these deposits in their USD equivalent. In this case, the exchange rate effect is calculated using the same formula. However, this time, the variables ERt and ERt-1 do not denote the original currency-denominated buying price of deposits but the dollar buying rate. The formula for this group of deposits is as follows:

For precious metal deposit accounts that are reported in terms of their TL equivalent in weekly reports, the exchange rate effect is obtained by calculating the net transaction over the USD equivalent of period-end stock amounts and deducting it from the total change. The calculation that employs the CBRT buying rate is as follows:

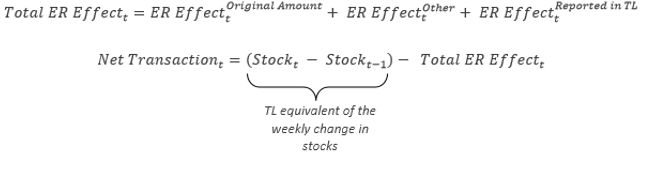

The total exchange rate effect and the net transaction within the money supply are calculated as follows:

Step 2: Calculation of the index of notional amounts[2]

Under this study, exchange rate-adjusted growth rates of money supply are calculated based on the “index of notional amounts” that excludes this effect and by taking the final week of 2014 as a basis. The index of notional amounts (INA) is formulated as follows:

The index thus calculated is defined as an analogous series independent of its unit. For example, a fall of the index from 100 to 90 means it has fallen by 10% between the two periods, when the money supply is adjusted for the exchange rate effect.

Growth rates are calculated via the index as follows:

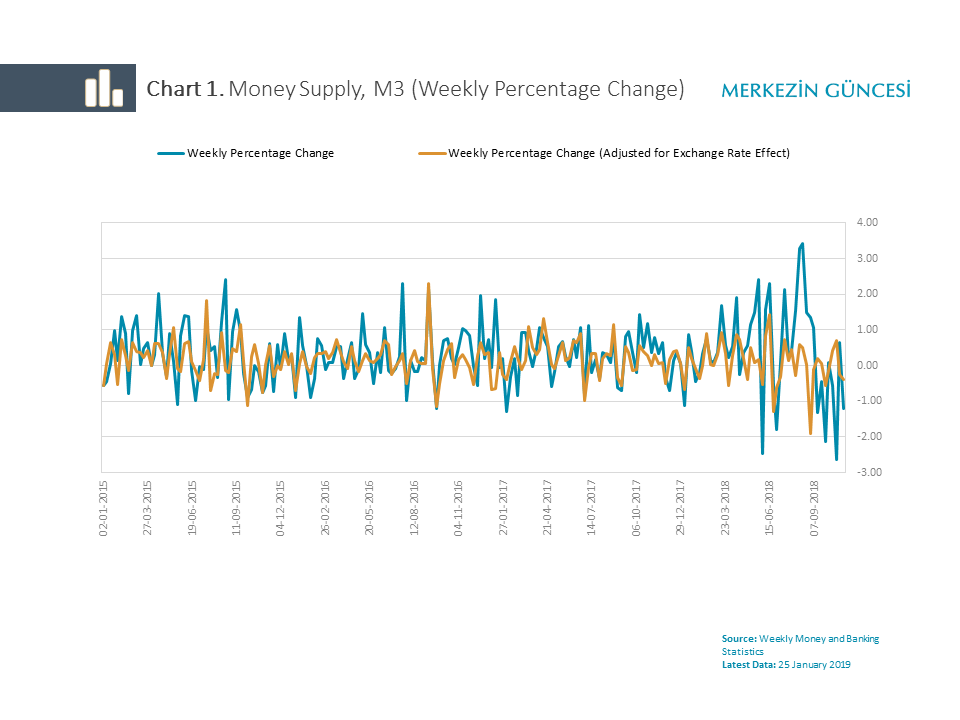

This formula denotes the weekly percentage change if s=1 and the annual percentage change if s=52. The charts below demonstrate the exchange rate effect for M3 as weekly and annual percentage changes.

To conclude, employing the methods defined above, we can answer the question “how would the movements in the money supply be if there were no fluctuations in exchange rates?” Charts suggest that the two series diverge more in periods of large fluctuations in exchange rates. In other words, when the exchange rate effect is ignored, the fluctuation in the money supply may seem larger than it actually is in periods of substantial changes in exchange rates, producing misleading signals. Actually, the sizable upward fluctuation in exchange rates observed in August 2018 constitutes the most recent example. During this period, the money supply registered a temporary increase whereas the exchange rate-adjusted series followed a flat course. In light of these examples, we believe that monitoring high-frequency money supply developments in both exchange rate-adjusted and non-exchange-rate-adjusted terms may be a better idea in economies with a high share of FX deposits in the money supply.

[1] Electronic Data Delivery System

[2] Calculations in this section are largely based on chapter 7.3 on “Index of notional stocks and growth rates” in the European Central Bank’s Manual on MFI balance sheet statistics.