İbrahim Ethem Güney is the Executive Director of the Strategy and Corporate Governance Department of the CBRT.

Forward foreign exchange contract is a type of derivative instrument actively used in financial markets to hedge against the exchange rate risk. The Central Bank of the Republic of Turkey (CBRT) has decided to launch Turkish lira (TL)-Settled Forward Foreign Exchange Auctions for the purpose of increasing depth in foreign exchange markets and supporting the effective management of the exchange rate risk of the corporate sector.

I. Use of Forward Foreign Exchange Contracts in Financial Markets

TL-Settled Forward Foreign Exchange contracts are a type of derivatives where the principal amounts are not exchanged between the parties on the settlement date and the transaction is based on the principle of cash settlement in TL. The use of this type of contracts has become very widespread in global financial markets and their share in derivatives markets has been increasing recently. According to the “Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity” conducted by the BIS, average daily transaction volumes of these instruments reached USD 134 billion in 2016[1].

Forward foreign exchange contracts are mainly used for the following purposes[2]:

- Firms’ hedging behavior against the exchange rate risk associated with their foreign currency (FX)-denominated liabilities;

- Hedging against interim FX payments,

- Hedging against the principal amount of FX liabilities with or without the need for foreign currency cash in the near term.

- Hedging of foreign investors’ local currency denominated assets against the exchange rate risk.

Among the purposes listed above, interim payments of the corporate sector are directly related to the foreign currency demand in the spot market. Other transactions are for hedging purposes and their natural environment is forward transactions. Empirical studies show that there is a mutual interaction between the forward foreign exchange transactions market and the spot market but the direction of the relationship is from forward towards spot market in periods of increased exchange rate volatility[3].

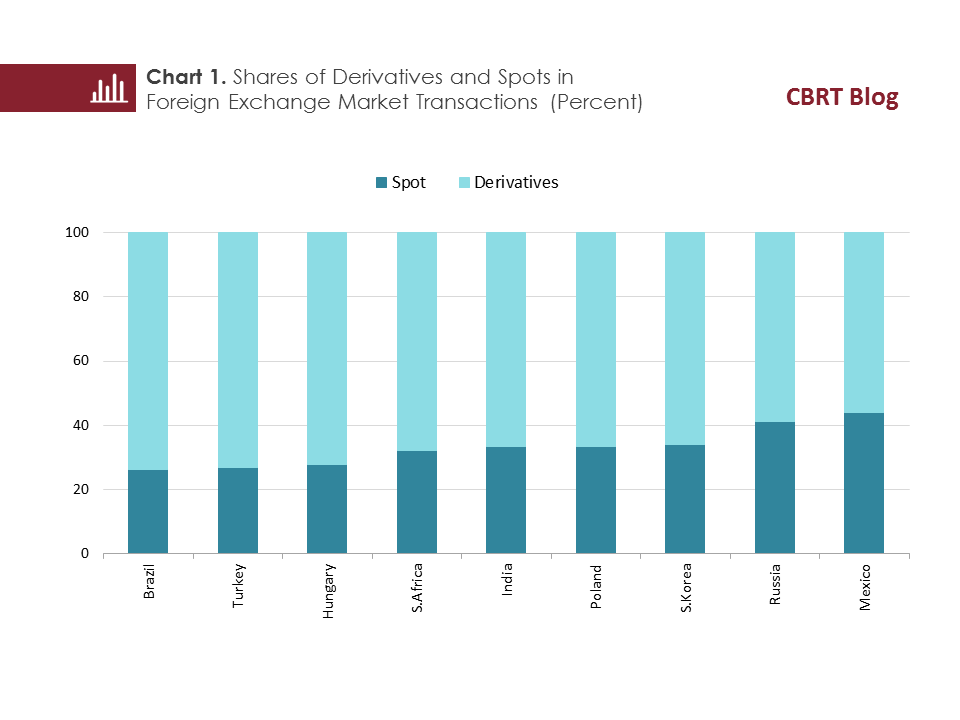

Data on global currencies presented in the “BIS Triennial Central Bank Survey” offer striking information about forward and spot foreign exchange transactions. It is noteworthy that a large portion of the total transaction volume in FX markets results from derivatives transactions such as forwards and swaps (Chart 1). This decomposition indicates that the majority of the transaction volume takes place for hedging purposes[4].

As explained above, increasing the depth in forward foreign exchange markets stands as a prerequisite for sustaining the FX market volatility at reasonable levels. In this respect, the TL-Settled Forward Foreign Exchange Auctions program announced by the CBRT is deemed a useful policy instrument in providing depth to the existing foreign exchange derivatives markets, which is crucial for the effective management of the corporate sector’s exchange rate risk and balancing excessive volatility in foreign exchange markets.

II. Mechanism of TL-Settled Forward Foreign Exchange Auctions

Forward foreign exchange contracts are derivative instruments which introduce a commitment to purchase or sell a specific currency against another one at an agreed forward exchange rate on a pre-determined settlement date.

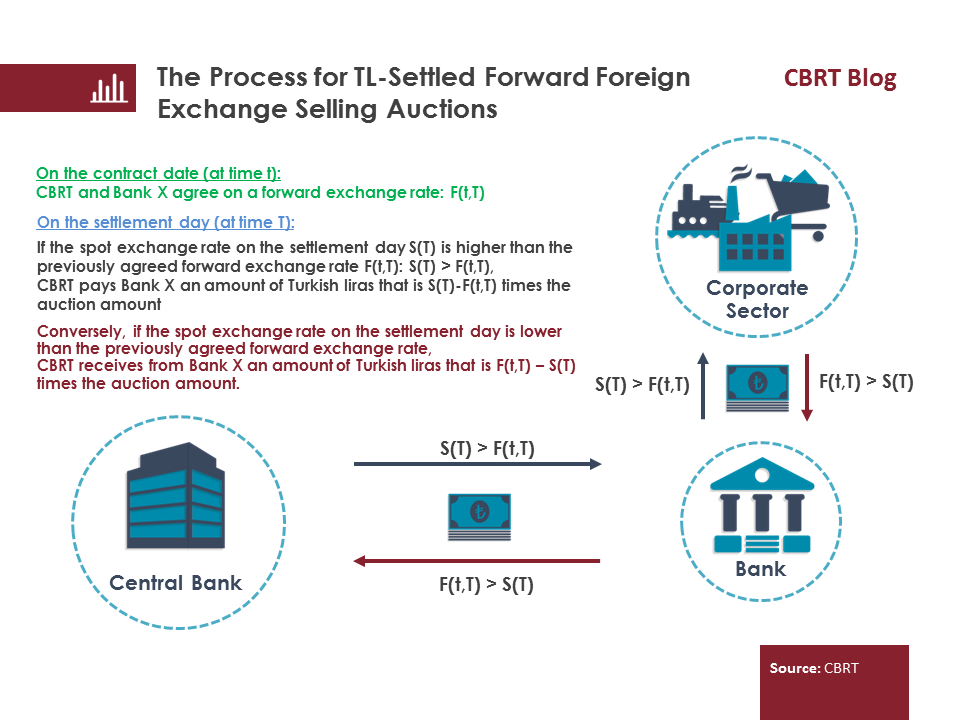

In the framework of the program recently shared with the public, the CBRT will be in FX-selling position in these auctions while the auction-winning banks will be in FX-buying position. Banks will be able to transfer these long FX positions to the corporate sector and/or to the markets abroad by undertaking a reverse position.

The position amount, forward price and the maturity are the key factors that need to be set on the contract day. In the framework of the TL-Settled Forward Foreign Exchange program, the CBRT will hold auctions at various maturities. The auctions will be held via the traditional (multi-price) auction method and banks that are members of the foreign exchange markets will be able to present their bids. Banks bidding in the auctions will submit the amount of foreign currency on which they would like to take a position and their forward exchange rate bid. The banks are obliged to keep collateral at the CBRT throughout the auction against any price and exchange rate changes. The winners of the auctions will be determined according to their forward exchange rate bids, thus the banks with the highest forward exchange rate bids will be the winners. The CBRT may also roll-over the maturing contracts if deems appropriate.

If the spot exchange rate on the maturity date is higher than the forward exchange rate set on the contract date, the CBRT will pay the difference between spot and forward exchange rate in TL. If the spot exchange rate on the settlement date is lower than the forward exchange rate set on the contract date, the CBRT will receive the difference between these two rates from the bidding bank. In neither case will payments on settlement dates be made in foreign currency.

III. Impact of TL-Settled Forward Foreign Exchange Auctions on CBRT’s Reserves and Profitability

TL-Settled Forward Foreign Exchange Auctions will have no impact on the CBRT’s foreign currency reserves. If the CBRT becomes the payer on the settlement date, the payment will be made in TL, so the CBRT will not draw down its foreign currency reserves. In the opposite case, the CBRT will become the receiver in TL.

In TL-Settled Forward Foreign Exchange auctions, the prices will be determined by supply-demand conditions within the market mechanism. In other words, prices in these auctions will be in tandem with the market prices. Accordingly, the impact of these auctions on the CBRT’s financial statements can be explained as follows. The CBRT carries a long US dollar position due to its net reserves. The CBRT generates foreign exchange profits when the US dollar appreciates against the Turkish lira. By definition, in TL-Settled Forward Foreign Exchange Auctions, the CBRT will be a net payer only when the US dollar appreciates against the Turkish lira. With this instrument, it will be as if the CBRT fixes the profit of a respective amount equal to the auction sum.

IV. What are the Potential Benefits of the Instrument?

The TL-Settled Forward Foreign Exchange Auctions will provide depth to the existing forward foreign exchange transactions in the financial markets. The CBRT will contribute to the increase in transaction volume and sustainability in the forward foreign exchange market as it will become a new actor by taking advantage of its foreign exchange net long position.

Banks will be able to transfer the forward foreign exchange long positions that they have purchased from the CBRT to the corporate sector through the over-the-counter markets in Turkey or sell them in foreign markets. In this respect, the new instrument will contribute to stabilizing the impact of the hedging behavior that increases at times of heightened FX volatility in domestic financial markets. The new instrument can also support price stability by underpinning current policies through the alleviation of the fluctuations in foreign exchange markets.

V. Conclusion

Data show that the bulk of foreign exchange transactions are of hedging needs whose natural environment is forward markets. Recent empirical studies suggest that there is a two-way interaction between the forward foreign exchange transactions and the spot market, nevertheless, at times of heightened FX volatility, the direction of the relation becomes “from the forward market towards the spot market”. Thus, increasing the depth of the forward market is considered an important prerequisite for sustaining the spot market volatility at reasonable levels.

The TL-Settled Forward Foreign Exchange Auctions are expected to support the corporate sector’s exchange rate risk management capacity by facilitating access to a simple, deep and efficient hedging instrument. Deepening of foreign exchange markets and efficient management of corporates’ exchange rate risk are in prospect to contribute to the monetary policy’s main objective of achieving and sustaining the price stability.

[1] BIS Triennial Central Bank Survey.

[2] Lipscomb, L. (2005).

[3] Chadha, B. (2017).

[4] McCauley, Shu and Ma (2014)

Bibliography

Chadha, B. (2017). “Understanding Non-Deliverable Forward (NDF) Markets and NDF Volatility Spillover to On-shore Indian Rupee Markets”, International Journal of Applied Business and Economic Research, Volume 15, Number 1.

Lipscomb, L. (2005), “An Overview of Non-Deliverable Foreign Exchange Forward Markets”, Federal Reserve Bank of New York, May.

McCauley, R. N., Shu, C., & Ma, G. (2014). “Non-Deliverable Forwards: 2013 and Beyond”, BIS Quarterly Review, March 2014.

İbrahim Ethem Güney is the Executive Director of the Strategy and Corporate Governance Department of the CBRT.